The Finnish affordable social housing sector plays a significant role in the development of a sustainable welfare state. In 2023, a vast majority of MuniFin’s housing loans were granted to either green or social finance projects.

An increasing amount of housing in Finland is being constructed and financed with consideration for social and environmental factors. Our customers, including affordable social housing organizations and municipal rental housing projects, play a significant role in this trend. Last year, the share of green and social finance in our housing loans reached a record high of 63 percent.

“An increasing number of our customers have made it their mission to carry out their projects more sustainably, taking into account environmental, climate or social benefits. Affordable social housing production is at the absolute forefront of sustainable construction in Finland”, says Päivi Petäjäniemi, Customer Relations Manager at MuniFin.

MuniFin was the first in Finland to start offering green finance for climate and environmentally friendly projects in 2016. In 2020, we also became the first to launch social finance, which emphasizes the social benefits of the projects: equality, communality, safety, welfare, or regional vitality.

“Our customers were among the first to learn about green and social finance, and we have persistently kept the topic on the agenda ever since. Nowadays, they have comprehensive knowledge of their alternatives, and they proactively seek green and social finance to give visibility to their projects. All their projects are significant for the Finnish welfare society, but the ones that fall under the green and social finance framework, are truly best in class”, Petäjäniemi explains.

Buildings and construction account for about a third of Finland’s greenhouse gas emissions*. The figures show that Finnish municipalities and non-profit housing operators are strongly involved in climate efforts.

The energy efficiency of affordable social housing buildings is generally higher than buildings in the private sector*. One factor is the forthcoming Corporate Sustainability Reporting Directive (CSDR), which is already directing the larger operators towards more sustainable choices. Also, the residents of newly constructed homes are increasingly demanding more energy-efficient housing solutions.

“More and more buildings are built in energy class A, which is the minimum demand in our green finance framework. Our customers are bold and want to try new things, so I expect to see a rising number of projects that also consider the impacts of the entire life cycle and construction chain. The challenge for now is that costs may seem higher in the construction phase. Saved energy costs for example, show in the long run, and our customers have strict demands for affordability from The Housing Finance and Development Centre of Finland (Ara), which oversees the projects.”

The prerequisites for the approval of social finance projects consider the social benefits of the projects.

“Our customers are increasingly planning housing as a whole, and this is clearly visible in projects for special groups. For example, they want to provide every student with their own apartment, but there is increasing investment in shared spaces, which promotes community and prevents loneliness. Residents are also offered various services, such as car-sharing or resident counselling”, Petäjäniemi says.

Finnish affordable social housing supports social mixing and brings down homelessness

In Finland, affordable social housing is mainly provided by municipality-owned companies and nationwide non-profit organisations. The production is financed through interest subsidy loans. The loans are guaranteed by the Finnish state through The Housing Finance and Development Centre of Finland (Ara), which is administered by the Ministry of the Environment. Alternatively, housing projects can also be loans to municipality owned companies. These loans do not have a state interest subsidy, but they come with a 100% municipal guarantee.

MuniFin is the main financier of affordable social housing production in Finland. The loan periods are long, up to 41 years.

The Finnish government updated its housing policy development programme in 2021. Some of the main objectives of this programme include increasing housing construction in growing urban areas and eradicating homelessness within two government terms. Affordable social housing has played a remarkable role in tackling homelessness in Finland, especially family homelessness. Affordable social housing is also instrumental in preventing segregation and facilitating labour mobility.

Our sustainability agenda sets the direction until 2035

As outlined in our strategy, key aspects of sustainability at MuniFin include acting as our customers’ partner in building a sustainable society while efficiently managing climate-related and environmental risks.

Our long-term impact stems from the products and services we offer our customers. In our sustainability agenda published in 2023, we set the direction and goals for our sustainability efforts until 2035.

In this agenda, we commit to increasing the proportion of sustainable finance in our lending portfolio into one third by 2030. In 2023, the share was 21,3 percent. We also set emission reduction targets for financed buildings. Our target level is 8 kgCO₂/m² by 2035, representing reduction compared to the 2022 level.

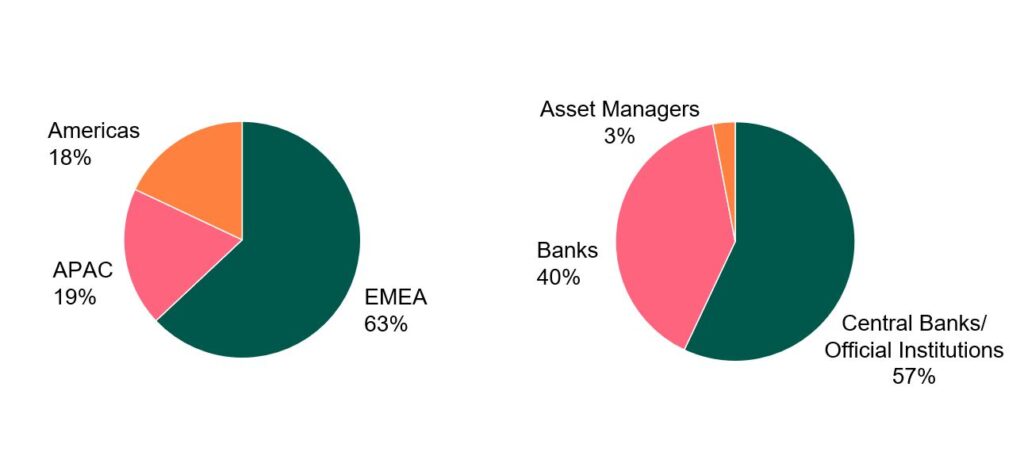

Three months following the record-breaking USD 1.5 billion issuance in January, MuniFin returns to the USD market with another 1 billion benchmark. The 3-year bond successfully gathered a high-quality orderbook.

On Tuesday 16 April, MuniFin issued a new 3-year USD 1 billion benchmark with initial price guidance of MS+33 basis points. Investor demand continued to grow throughout the morning and books closed a few hours later in excess of USD 1.5 billion.

The bond was priced at MS +33 basis points, consistent with the initial guidance, with a coupon of 4.875%, a reoffer price of 99.708% and a re-offer yield of 4.981%. It carries a spread of 18 basis points over the CT 3 4.500% due 15 April 2027.

The final orderbook was geographically diverse with 48 high-quality accounts participating. Central banks took 57% of the allocations, followed by Banks and bank treasuries (40%), and Asset Managers, taking the remaining 3%.

“Investor demand started to accumulate after a moderate start, eventually reaching over USD 1.5 billion. We were particularly pleased with the quality of the final orderbook, as majority was allocated to central banks and official institutions. We have now successfully secured a little less than half of our funding target for the year”, says Analyst Aaro Koski.

After this transaction, MuniFin has now completed EUR 4.5 billion of its EUR 9–10 billion funding programme for 2024.

Aaro Koski, Analyst at MuniFin’s Funding and Sustainability team.

Distribution

Transaction details

Issuer:

Municipality Finance Plc (“MuniFin”)

Rating:

Aa1 / AA+ (Moody’s/S&P – both stable)

Issue Size:

USD 1 billion

Payment Date:

23 April 2024 (T+5)

Maturity Date:

23 April 2027

Coupon:

4.875%

Re-offer Price:

99.667%

Re-offer Yield:

4.996%

Re-offer vs. Mid Swaps:

+33bps

Re-offer vs. Benchmark:

CT 3 4.500% due 15 April 2027 +18bps

ISIN:

XS2807531657 / US62630CEL19

Lead Managers

J.P. Morgan SE, Morgan Stanley Co & International PLC, Nomura Financial Products Europe GmbH, TD Global Finance unlimited company

Comments from Lead Managers

Ben Adubi, Managing Director, Head of SSA, Morgan Stanley:

“Another successful outing in the USD market for MuniFin following their strong 5-year issued earlier this year. Taking advantage of the favourable move in swap spreads and recent sell-off in rates, the deal amassed a high-quality and granular orderbook with 57% of allocations to CB/OIs, which is a testament to the strength of MuniFin’s credit quality and their opportunistic funding strategy. Congratulations to the MuniFin team on a stellar start to Q2, following on from an impressive start to the year, Morgan Stanley is delighted to have been involved!”

Mark Yeomans, Managing Director, Nomura:

“Yet another strong USD outing from MuniFin; with the new 3-year benchmark complementing the 5-year issued earlier in January. MuniFin took advantage of the global back up in rates to deliver another record 4.875% coupon for investors, as witnessed in their previous 3-year from last October. The quality of the orderbook is a testament to the investor following that MuniFin enjoys as a safe haven asset and the diligent investor outreach of the entire funding team. Nomura were delighted to be a part of such an important transaction.”

Ioannis Rallis, Executive Director, Head of SSA DCM, J.P. Morgan:

“Congratulations to the MuniFin team for printing another solid USD benchmark this year! Despite uncertain geopolitical backdrop and busy pipeline in the week, MuniFin was successfully able to achieve its tightest spread vs SOFR MS (+33bps) for a MuniFin USD 3-year benchmark. The high quality of the orderbook reflected in the 57% allocation to CB/OIs is a testament to investor confidence in MuniFin’s name. We are delighted to be involved in this transaction.”

Laura Quinn, Managing Director, Global Co-Head of SSA and Head of Dublin Debt Capital Markets:

“Congratulations to the MuniFin team on a successful USD benchmark transaction, launching their first 3-year USD benchmark in 2024 and second USD benchmark this year. MuniFin secured an efficient funding window this week to ensure they could complete their USD 1 billion funding exercise. The exceptionally high-quality orderbook is a testament to MuniFin’s standing in the fixed income market.”

MuniFin is part of a Nordic public sector issuer group that has released a new edition of the Position Paper on Green Bonds Impact Reporting. The updates to these reporting recommendations stem from recent market developments, especially from emission reductions in energy production.

Published by Nordic public sector issuers, the Position Paper on Green Bonds Impact Reporting is a practical guide to reporting the environmental impact of projects financed through green bonds. It includes impact indicators, calculation methods and reporting practices.

“The material changes in the 2024 update include revised emission factors for electricity and district heating, new recommendations for vintage reporting and more specific recommendations on topics such as look-back/allocation periods, refinancing, ESG strategy and risk management”, says MuniFin’s Sustainability Manager Mikko Noronen.

In the latest edition of the position paper, the issuer group revised the emission factors for electricity and district heating downwards to reflect the energy sector’s rapid transition towards fossil-free energy sources.

Nordic recommendations harmonise the green bonds market

The purpose of the Nordic reporting recommendations is to create harmonious and transparent green bonds impact reporting principles that cultivate market practices. This allows issuers to report on the environmental impact of their financed projects in a way that offers investors high-quality information that is comparable, transparent and also supports the investors’ own reporting.

“For sustainable bonds to retain and strengthen their credibility as useful tools to finance the transition, it is of importance that market participants undertake issuance and reporting in a diligent and transparent manner”, says Björn Bergstrand, Head of Sustainability at Sweden’s Kommuninvest and coordinator of the Nordic cooperation.

Developed to assist Nordic public sector borrowers in reporting the environmental impact from their investments, the Position Paper on Green Bonds Impact Reporting has come to be used by issuers also in the private sector.

The Position Paper on Green Bonds Impact Reporting was first introduced in 2017 and is now in its fourth edition.

The Nordic public sector issuer group publishing the Position Paper on Green Bonds Impact Reporting includes MuniFin and MuniFin’s Nordic public sector counterparts, Kommunalbanken in Norway, KommuneKredit in Denmark and Kommuninvest in Sweden, as well as the Swedish Export Credit Corporation (SEK) and a number of Swedish municipal and regional issuers.

We have published our annual report for 2023. We have also published the impact reports on our green and social finance and the Pillar III disclosure report on capital adequacy.

The year 2023 was the fourth consecutive year marked by instability. In these uncertain times, our role as our customers’ trusted financing partner has grown even more important. At MuniFin, 2023 was a year when we put sustainability even more front and centre as we revised our strategy and published our first sustainability agenda.

The volatile operating environment did not significantly affect our performance. Our operations remained stable, and we were again able to successfully carry out our core mandate of providing affordable long-term financing for our customers.

Our long-term customer finance increased by about 10% from the previous year. Our new long-term customer financing remained on a par with 2022, totalling EUR 4.4 billion. Our profitability was slightly higher than in 2022.

The amount of our sustainable finance, i.e. our green and social finance, grew by about EUR 2 billion in 2023. Our sustainable finance products are our way of encouraging our customers to make more responsible investments. Read more about the impacts of our sustainable finance in the green and social impact reports published today.

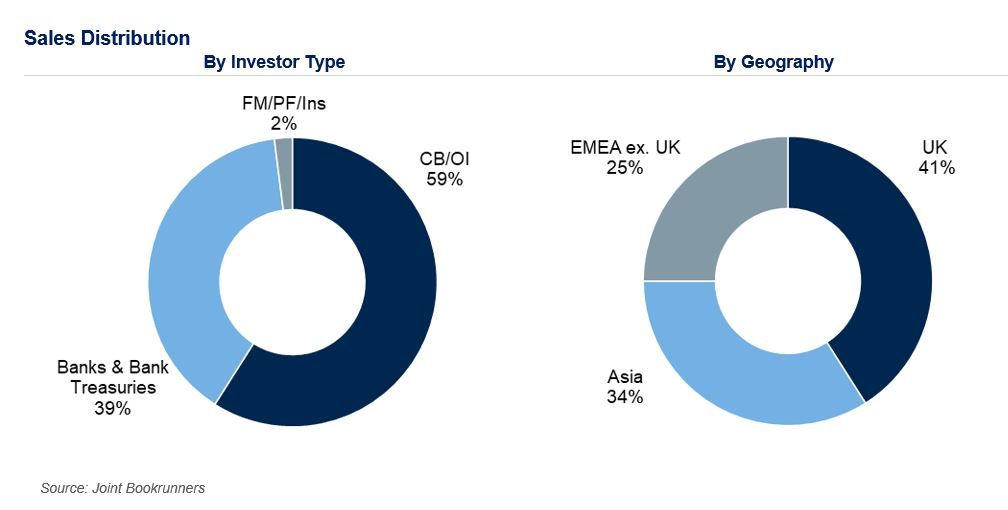

MuniFin’s GBP 250 million issue on February 29 was well received in the market, with particularly strong participation from central banks and official institutions. With this transaction, MuniFin has now printed one third of its EUR 9–10 billion funding programme for the year 2024.

Distribution of the transaction was once again broad both in terms of investor types and geographics, which is testament to MuniFin’s strong position in the global investor community.

Central banks and official institutions were the largest investor component, taking 59% of the final book. The participation was also strong from banks and bank treasuries (39%), with fund managers, pension funds and insurance accounts representing 2%. In terms of geography, the transaction was broadly diversified across UK (41%), Asia (34%) and EMEA ex. UK (25%) investors.

“This was our first GBP line of the year, and it was great to extend our GBP issuance curve today. We are grateful for the investor following we have in the Sterling market and it has been a pleasure to be able to be on the screens again”, says Senior Manager Karoliina Kajova from MuniFin’s funding and sustainability team.

“Congratulations to the MuniFin team for a strong return to the GBP market, taking advantage of a clear issuance window to extend their GBP curve with a new benchmark. The strong support from a diverse group of investors and the competitive price point is a testament to MuniFin’s standing in the international market. We’re delighted to be involved!” Tina Nguyen, Vice President, SSA DCM, J.P. Morgan

“Congratulations to the MuniFin team on the new GBP Oct-28 Benchmark. Taking advantage of a clear issuance window, MuniFin were able to extend their GBP Benchmark curve and maintain their regular presence in the Sterling SSA market. RBC were delighted to be a part of the transaction.” James Taunton, Director, SSA DCM, RBC Capital Markets

“We are delighted to be involved in MuniFin’s successful return to the Sterling market with their first GBP Benchmark of the year. This syndication is a clear demonstration of their global support from a diversified investor base. Congratulations to the MuniFin team on an excellent trade.” Paul Eustace, Managing Director, Global Co-Head of SSA and Head of Europe and Asia Syndicate, TD Securities

Further information

Joakim Holmström Executive Vice President, Capital Markets and Sustainability +358 50 4443 638

Antti Kontio Head of Funding and Sustainability +358 50 3700 285

Originating from the vision of children, the Tuusula-based Martta Wendelin Daycare Centre embodies respect for children and sustainable development.

Since the summer of 2022, this exceptional building has added life to the scenery of the municipality of Tuusula in Southern Finland. The Martta Wendelin Daycare Centre, designed with children’s needs in mind, won the prestigious Finlandia Prize for Architecture for its distinctive architecture and execution.

User-oriented approach and ecological values steered the project

As part of the service network design in 2018, Tuusula resolved to replace several old daycare centres with new buildings. Stemming from a vision of preschoolers, the Martta Wendelin Daycare Centre was established, resulting in a new daycare centre in Tuusula with 10 groups, providing about 200 daycare places for children.

“The idea for the daycare centre was born when we started sketching a vision of the dream playground together with preschool-aged children. Later, the Martta Wendelin Society joined the project. This was natural, as the artist Martta Wendelin, known for her depictions of Finnish rural and home life, spent most of her life right here in Tuusula,” recalls Tiina Simons, Director of Education in Tuusula, about the early stages of the project.

Martta Wendelin’s art is also a prominent part of the daycare’s interior decoration.

“The entire project has been carried out using user-centred design. The history of Tuusula has been brought into the building in a skillful and beautiful manner,” says Pirjo Sirén, Director of Municipal Development.

Significant efforts have been made in the implementation of the Martta Wendelin Daycare to utilise environmentally friendly solutions and climate-smart construction. This can be seen, for example, in the energy efficiency and in the way the principles of the circular economy have been taken into account both during the construction phase and in the planning of the building’s life cycle.

Thanks to its environmental friendliness, the project has been financed with green finance from MuniFin.

“Although the high-quality implementation of the daycare required a significant investment, we expect to achieve savings on the operating budget side. Combining four early education units into one makes the organization of operations more cost-effective and the maintenance of the property easier,” says Markku Vehmas, the acting Chief of Staff of the municipality.

Children and nature come first

The Martta Wendelin Daycare Centre embodies respect for the environment and sustainable development. The building has been constructed with materials that prioritise environmental friendliness and health.

“The structures of the exterior and interior walls as well as the intermediate floors have used CLT massive construction that acts as a carbon sink. The design of the spaces has focused on diversity and flexibility so that they can serve different purposes. The yard designed for play and exercise beautifully opens to the south. Part of the forest has also been left on the yard area to be preserved, as well as a stormwater puddle where children can jump to their heart’s content in rainy weather,” Sirén describes.

“The building has also not been filled with colors or artworks. The wooden surfaces create frames into which the children can bring colors,” Simons continues.

The exceptional nature of the building has brought various recognitions to the municipality. In addition to the Finlandia Prize for Architecture, the daycare centre has also won the 2023 International Award for Wood Architecture, awarded by five European architectural journals.

“I also consider the awards as a tribute to our high-quality early childhood education,” Simons states.

Most importantly, positive feedback has been received from the users of the building.

“We have received particular praise for the brightness and spaciousness of the spaces. Children love being at the daycare and enjoy themselves both indoors and in the yard activities,” Simons rejoices.

Finance for Finland's green transition

MuniFin has offered its customers green finance for sustainable investments since 2016. Funding for green projects is sourced by issuing green bonds. For investors, MuniFin’s green bonds offer a way to finance positive impacts through carefully selected projects in e.g. buildings, transportation and renewable energy categories.

MuniFin’s inaugural NOK social bond was issued on 13 February. Despite ample supply from SSA issuers in the NOK market, the demand for the NOK 2 billion issue was strong, with a high quality investor base.

The issue marked both MuniFin’s first ESG labelled bond and the first NOK trade this year. The books built very quickly and were closed at a spread of +25 bps over 3-month Nibor.

“Over the past years, MuniFin has established themselves as a frequent issuer in the Nordic market, popular amongst a wide array of investors. The new issue marks the first social bond issued by MuniFin in Norway and the label was a significant contributor to the great investor demand”, says Hedda Giæver, Head of IG International, DBN Bank ASA.

The strong investor base showcased significant interest from bank treasuries, as well as domestic and foreign real money, including pension insurance and asset managers.

80% of the issue was allocated to Norwegian investors.

“We are extremely happy to have been able to return to the Norwegian Krona market. What’s even more pleasing is to be able to do it with a social bond. It is in the very core of our Sustainability Agenda to provide financing to social projects and increase their share in our lending portfolio. We are ever grateful for the support from our investors”, says Aaro Koski, MuniFin’s Funding Analyst.

Transaction details

Issuer:

Municipality Finance (KUNTA, MuniFin)

Issue Rating:

Aa1/AA+

Status:

Senior unsecured

Reoffer Price:

99.631% / 4.083%

Reoffer Spread:

3mN+25bps

Issue Size:

NOK 2bn

Settlement:

20 February 2024

Maturity:

20 February 2029

Coupon:

4% Fixed, Annual, Act/Act Icma Unadjusted Following

Listing:

Nasdaq Helsinki

ISIN:

XS2769883955

Lead Manager:

DNB Markets

Further information

Joakim Holmström, Executive Vice President, Capital Markets and Sustainability, +358 50 4443 638 Antti Kontio, Head of Funding and Sustainability, +358 50 3700 285 Karoliina Kajova, Senior Manager, Funding, +358 50 5767 707 Lari Toppinen, Senior Analyst, Funding, +358 50 4079 300 Aaro Koski, Analyst, Funding, +358 45 138 746

The Group’s net operating profit excluding unrealised fair value changes in January–December increased by 3.2% and amounted to EUR 176 million (EUR 170 million). The net interest income grew by 7.5% propelled by rising short-term market rates and totalled EUR 259 million (EUR 241 million). The growth in result was slowed down by an increase in costs.

Net operating profit amounted to EUR 139 million (EUR 215 million). Unrealised fair value changes amounted to EUR -37 million (EUR 45 million) in the financial year. Unrealised fair value changes were influenced in particular by changes in interest rate expectations and credit risk spreads in the Group’s main funding markets.

Costs in the financial year amounted to EUR 82 million (EUR 73 million). The growth in costs was primarily driven by the almost quadrupled guarantee commission of EUR 13 million (EUR 4 million) paid to the Municipal Guarantee Board, which resulted from a change in the calculation method. The guarantee commission is a compensation for the guarantees the Municipal Guarantee Board grants to MuniFin’s funding.

The Group’s leverage ratio continued to strengthen, standing at 12.0% (11.6%) at the end of December.

At the end of December, the Group’s CET1 capital ratio was very strong at 103,4% (97.6%). CET1 capital ratio was well over the total requirement of 13.9%, with capital buffers accounted for. Because MuniFin Group only has CET1 capital, Tier 1 and total capital ratios are the same with the CET1 capital ratio, 103.4% (97.6%).

The Russian invasion of Ukraine has not had a significant effect on the Group’s operations. The war has accelerated inflation and pushed up market interest rates, which has had a positive effect on the Group’s net interest income, but also increased costs. Because of the geopolitical uncertainty caused by the war, the Group has maintained strong liquidity buffers. Otherwise, the war has had only a minor effect on the Group’s operations.

Long-term customer financing (long-term loans and leased assets) excluding unrealised fair value changes totalled EUR 32,948 million (EUR 30,660 million) at the end of December and saw an increase of 7.5% (5.5%). New long-term customer financing in January–December was at the same level as in the previous year and amounted to EUR 4,370 million (EUR 4,375 million). Short-term customer financing totalled EUR 1,575 million (EUR 1,457 million).

Of all long-term customer financing, the amount of green finance aimed at environmentally sustainable investments totalled EUR 4,795 million (EUR 3,251 million) and the amount of social finance aimed at investments promoting equality and communality totalled EUR 2,234 million (EUR 1,734 million) at the end of December. The total amount of this financing increased by 41.0% (42.9%) from the previous year. The ratio of green and social finance to long-term customer financing excluding unrealised fair value changes grew by 5.1 percentage points to 21.3%. In late 2023, the Group published its sustainability agenda, which extends to the year 2035. By the end of 2030, the Group’s goal is to increase the share of green and social financing to one third of all long-term customer financing, and by the end of 2035 reduce emissions from financed properties by 38% from the 2022 level.

In 2023, new long-term funding reached EUR 10,087 million (EUR 8,827 million). At the end of December, the total funding was EUR 43,320 million (EUR 40,210 million), of which long-term funding made up EUR 39,332 million (EUR 35,560 million). In March and in June 2023, the Group decided to repay the debt related to the European Central Bank’s targeted longer-term refinancing operations (TLTROIII). The debt totalled EUR 2,000 million.

The Group’s total liquidity remained very strong, standing at EUR 11,633 million (EUR 11,506 million) at the end of the financial year. The liquidity coverage ratio (LCR) stood at 409% (257%) and the net stable funding ratio (NSFR) at 124% (120%) at the end of the year.

The Board of Directors proposes to the Annual General Meeting to be held in spring 2024 a dividend of EUR 1.69 per share, totalling EUR 66.0 million. The total dividend payment in 2023 was EUR 1.73 per share, totalling EUR 67.6 million.

Outlook for 2024: The Group expects its net operating profit excluding unrealised fair value changes to be at the same level or higher than in 2023. The Group expects its capital adequacy ratio and leverage ratio to remain strong. The valuation principles set in the IFRS framework may cause significant but temporary unrealised fair value changes, some of which increase the volatility of net operating profit and make it more difficult to estimate. A more detailed outlook is presented in the section Outlook for 2024.

Comparison figures deriving from the income statement and figures describing the change during the reporting period are based on figures reported for the corresponding period in 2022. Comparison figures deriving from the balance sheet and other cross-sectional items are based on the figures of 31 December 2022 unless otherwise stated.

Key figures

Jan–Dec 2023

Jan–Dec 2022

Change, %

Net operating profit excluding unrealised fair value changes (EUR million)*

176

170

3.2

Net operating profit (EUR million)*

139

215

-35.5

Net interest income (EUR million)*

259

241

7.5

New long-term customer financing (EUR million)*

4,370

4,375

-0.1

New long-term funding (EUR million)*

10,087

8,827

14.3

Cost-to-income ratio, %*

32.4

23.9

35.7

Return on equity (ROE), %*

6.6

9.9

-33.5

31 Dec 2023

31 Dec 2022

Change, %

Long-term customer financing (EUR million)*

32,022

29,144

9.9

Balance sheet total (EUR million)

49,736

47,736

4.2

CET1 capital (EUR million)

1,550

1,482

4.6

Tier 1 capital (EUR million)

1,550

1,482

4.6

Total own funds (EUR million)

1,550

1,482

4.6

CET1 capital ratio, %

103.4

97.6

5.9

Tier 1 capital ratio, %

103.4

97.6

5.9

Total capital ratio, %

103.4

97.6

5.9

Leverage ratio, %

12.01

11.6

3.8

Personnel

185

175

5.7

* Alternative performance measure. All figures presented in the Financial Statements Bulletin are those of MuniFin Group, unless otherwise stated

Comment on the 2023 financial year by President and CEO Esa Kallio

The year 2023 was the fourth consecutive year marked by instability. The rising geopolitical tensions and market volatility did not significantly affect MuniFin’s performance, and we were able to successfully carry out our core mandate of ensuring the availability of affordable long-term financing for our customers.

In 2023, the inflation exacerbated by the Russian invasion of Ukraine in 2022 took a downward turn, and interest rate hikes tapered off. Geopolitical tensions increased across the world throughout the year, and expectations of central bank measures caused uncertainty in the capital markets.

In Finland, the first half of the year was characterised by the parliamentary elections held in April and the ensuing government formation talks that stretched into June. The new government programme is unlikely to affect municipal operations directly. In the housing sector, our customers have been concerned about the government programme’s entries concerning right-of-occupancy housing and state-subsidised housing production. In this uncertain operating environment, our role as our customers’ trusted partner has grown even more important.

The demand for financing from our customers in the municipality sector was quiet at the beginning of the year, but demand picked up towards the end of the year close to the previous year’s level. Temporary tax benefits boosted municipal finances, causing municipalities to have lower financing needs. In municipal finances, 2023 was still a relatively good year, but started to weaken at the end of the year.

In the affordable social housing sector, financing needs were higher than in the year before. Our housing sector customers have suffered from rising construction costs for several years now, which has decreased the start of new building contracts. Rising interest expenses have taken a further toll on them since 2022. Towards the end of the year, however, the demand for financing started to pick up as construction costs levelled off and right-of-occupancy project starts were rushed because of the new government programme’s entries.

The new wellbeing services counties started their operations on 1 January 2023, and we financed the wellbeing services counties within the limits set by the Municipal Guarantee Board (MGB). The EUR 400 million limit for long-term finance set by the MGB was reached before the end of the year, and we could no longer fulfil wellbeing services counties’ financing requests for 2023 after that.

Our funding operations were a success despite the fluctuation in the capital markets. Our issuances were well-timed, and all our transactions were successful. We continued to keep our liquidity at a strong level throughout the year to ensure the availability of financing for our customers in all conditions.

Our operations continued in the usual manner in 2023, and our profitability was slightly higher than in 2022.

In 2023, we revised our strategy to further underline our core mandate. Our revised strategy highlights sustainability and our role as an enabler of sustainable welfare in society. We also made efforts to better assess and measure the impact of our operations. In October, we published our sustainability agenda, which sets the framework and goals for our long-term sustainability work. The agenda focuses on our business operations, i.e. the products and services offered to our customers, and the long-term impact achieved through them.

Outlook for 2024

The global economy is starting 2024 in a weakening economic cycle. The demand-slowing effects of interest rate hikes are reaching their peak and making sources of growth scarce, while fiscal policies are contracting as governments need to curb their debt. The geopolitical environment continues to remain unpredictable. On the upside, the cooling economy is helping to cushion cost pressures, and inflation is falling towards the ECB’s target of 2% in the euro area. The ECB is expected to commence interest rate cuts in 2024.

In Finland, the combined effect of factors saddling growth will peak in the first half of 2024. As the months pass and inflation eases, consumer purchasing power increases and interest rates start to come down moderately, the domestic market will gradually kick off economic recovery. Towards the end of the year, the export market may also start to contribute to recovery. Because of the low starting level, Finland’s GDP growth may nevertheless remain slightly in the negative in 2024.

The economic downturn will inevitably reflect on employment. In many sectors, Finland is suffering from such high structural labour shortages that strong growth in unemployment seems unlikely, but the employment outlook is nevertheless looking risky. It remains difficult to estimate how severe the construction sector’s recession will become and what multiplier effects this will have in other sectors. The euro area’s inflation trajectory is also looking somewhat uncertain. If inflation proves more persistent than anticipated and expected interest rate cuts are postponed, the downturn may drag on and push unemployment up more than expected.

Although Finland’s government programme sports ambitious fiscal efforts, public finances are projected to continue to show a significant deficit and high levels of debt in the coming years. The higher-than-expected increase in health and social services expenditure and financing costs and the cyclical decrease in tax income are making public finances difficult to balance. After a few exceptionally strong years, the municipal sector will return into serious deficit as various positive non-recurring items cancel out, costs increase and central government transfers decrease. The main uncertainties in municipal finances stem from the general economic development, the upcoming changes to central government transfers and the potential additional costs arising from the transfer of employment and economic development services (TE services) to municipalities.

Considering the above-mentioned circumstances, the Group expects its net operating profit excluding unrealised fair value changes to be at the same level as or higher than in 2023. The Group expects its capital adequacy ratio and leverage ratio to remain strong. The valuation principles set in the IFRS framework may cause significant but temporary unrealised fair value changes, some of which increase the volatility of net operating profit and make it more difficult to estimate.

These estimates are based on a current assessment of the development of MuniFin Group’s operations and the operating environment.

Municipality Finance Plc

Further information:

Esa Kallio, President and CEO, tel. +358 50 337 7953 Harri Luhtala, Executive Vice President, Finance, CFO, tel. +358 50 592 9454

Download the full Financial Statements Bulletin 1 January–31 December 2023

MuniFin’s annual report 2023 will be published around 7 March 2024. On the same date, MuniFin Groupwill also publish the Pillar III disclosure based on the Capital Requirements Regulation, and the Corporate Governance Statement.

MuniFin’s net operating profit excluding unrealised fair value changes amounted to EUR 74 million in the first half of the year. A year before the figure was a record-high EUR 108 million. This year’s drop was expected, as it was influenced by the change in credit terms applied in late 2021.

New lending in January–June amounted to approximately EUR 2 billion and the long-term customer financing excluding fair value changes grew by 2.6% and totalled EUR 29.8 billion.

The amount of green finance aimed at environmentally sustainable investments totalled EUR 2,700 million (EUR 2,328 million) and the amount of social finance aimed at investments promoting equality and communality EUR 1,296 million (EUR 1,161 million) at the end of June.

In January–June, new long-term funding reached EUR 5,962 million (EUR 6,025 million). Group’s consolidated statement of financial position grew to EUR 47.5 billion.

– The pandemic has transformed our lives into something that is predicted to become the new normal, but the outlook has become even murkier than expected after the war broke out in Europe. Amidst all this uncertainty, it is important to note that at MuniFin, we work hard every day to create stability in these uncertain times and to ensure smooth operations for all our customers, notes Esa Kallio, President and CEO at MuniFin.

At the end of June, the MuniFin’s capital ratio was very strong. The Group will also publish a separate Pillar III Report on risk management and capital adequacy on August 8.

The Group’s net operating profit excluding unrealised fair value changes amounted EUR 213 million (EUR 197 million) and it increased by 8.0% (6.2%). The Group’s net interest income totalled EUR 280 million (EUR 254 million) and grew by 10.3% (5.8%). Costs in the financial year amounted to EUR 72 million (EUR 58 million). Costs excluding the non-recurring item grew as expected and were EUR 2.6 million higher, making the figure 4.4% greater than in the previous year.

The net operating profit amounted to EUR 240 million (EUR 194 million). Unrealised fair value changes amounted to EUR 27 million (EUR -3 million) in the financial year.

Changes to the regulation of banks’ capital adequacy (CRR II and CRD V) were applied at the end of June 2021. The Group’s leverage ratio was 12.8% (3.9%) at the end of December. MuniFin fulfils the CRR II definition of a public development credit institution and may therefore deduct all credit receivables from the central government and municipalities in the calculation of its leverage ratio. This change explains the growth of leverage ratio.

At the end of December 2021, the Group’s CET1 capital ratio remained very strong, 95.0% (104.3%). Tier 1 and total capital ratio were 118.4% (132.7%). The new CRR II regulation lowered the capital ratio mainly due to the changes in the calculation of the counterparty credit risk and CVA VaR. CET1 capital ratio nevertheless exceeded the total requirement of 13.4% by over seven times, with capital buffers accounted for.

The COVID-19 pandemic that broke out in March 2020 has now lasted almost two years, although its intensity has varied. As a whole, the pandemic has only had a minor effect on the Group’s financial standing. In this financial year, the demand for financing in the municipal sector remained lower than expected due to surprisingly good economic development and the Government’s temporary COVID-19 recovery measures in 2020.

Long-term customer financing, including both long-term loans and leased assets totalled EUR 29,214 million (EUR 28,022 million) and grew by 4.3% (13.0%) at the end of December. The total of new lending in January–December amounted to EUR 3,275 million (EUR 4,764 million). Short-term customer financing decreased by 16.9% (previous year’s growth was 62.9%) and reached EUR 1,089 million (EUR 1,310 million).

Of all long-term customer financing, the amount of green finance aimed at environmentally sustainable investments totalled EUR 2,328 million (EUR 1,786 million) and the amount of social finance aimed at investments promoting equality and communality totalled EUR 1,164 million (EUR 589 million) at the end of December. Green and social finance have been well received by customers, and the amount of this finance increased by 47.0% (88.0%) from the previous year.

In 2021, new long-term funding reached EUR 9,395 million (EUR 10,966 million). At the end of December, the total amount of acquired funding was EUR 40,712 million (EUR 38,139 million), of which long-term funding made up for EUR 36,893 million (EUR 34,243 million).

The Group’s liquidity has remained at a very good level. At the end of December, total liquidity amounted to EUR 12,222 million (EUR 10,089 million). The Liquidity Coverage Ratio (LCR) stood at 334.9% (264.4%) at the end of the year and the Net Stable Funding Ratio (NSFR) at 123.6% (116.4%).

The Board of Directors proposes to the Annual General Meeting to be held in spring 2022 a dividend of EUR 1.03 per share for 2021, totalling EUR 40,235,711.94. The total dividend payment for 2020 was EUR 20,313,174.96.

Outlook for 2022: The Group expects its net operating profit excluding unrealised fair value changes to be significantly lower than in the previous year, as per the Group’s long-term profitability targets and more beneficial customer pricing enabled by these targets. The Group expects its capital adequacy ratio and leverage ratio to remain very strong. The valuation principles set in IFRS 9 may cause significant but temporary unrealised fair value changes, some of which increase the volatility of net operating profit and make it more difficult to estimate in the short term.

Key figures (Group)

31 Dec 2021

31 Dec 2020

Net operating profit excluding unrealised fair value changes (EUR million)*

213

197

Net operating profit (EUR million)*

240

194

Net interest income (EUR million)*

280

254

New lending (EUR million)*

3,275

4,764

Long-term customer financing (EUR million)*

29,214

28,022

New long-term funding (EUR million)*

9,395

10,966

Balance sheet total (EUR million)

46,360

44,042

CET1 capital (EUR million)

1,408

1,277

Tier 1 capital (EUR million)

1,756

1,624

Total own funds (EUR million)

1,756

1,624

CET1 capital ratio, %**

95.0

104.3

Tier 1 capital ratio, %**

118.4

132.7

Total capital ratio, %**

118.4

132.7

Leverage ratio, %**

12.8

3.9

Return on equity (ROE), %*

10.7

9.4

Cost-to-income ratio*

0.2

0.2

Personnel

164

165

*Alternative performance measure. **Figures for the financial year 2021 are calculated in accordance with CRR II. Comparison periods have not been restated to reflect the updated capital requirements regulation.

Comment on the 2020 financial year by President and CEO Esa Kallio

Finland’s economic and employment situation exceeded expectations in 2021 and reached a surprisingly good level. The central government’s COVID-19 support package ensured that municipalities have not had to shoulder the negative economic effects of the pandemic.

Municipal sector’s demand for financing was lower than expected in 2021. The demand for state-subsidised housing finance grew moderately, as expected. MuniFin’s market position is strong, and we continue to be by far the largest single credit institution offering long-term loans for our customer base.

Despite the temporarily improved financial situation, the fiscal sustainability gap and structural problems in the public economy continue to exist. In 2022, we therefore expect the demand for financing in the municipal sector to return to the pre-pandemic level.

The European Union’s changes to the capital adequacy regulation were applied at the end of June. Under the new regulation, MuniFin gained the status of a public development credit institution, which significantly eases MuniFin’s ability to comply with the leverage ratio capital requirement. This has allowed us to increasingly transfer the benefit from negative interest rates to our customers, making our loan financing even more affordable than before. This change in our credit terms took force in October, and its benefits will begin to have a wider impact in the interest expenses of our loan customers in 2022.

Once again, our funding succeeded excellently, and the availability of funding in the international capital market remained good. Thanks to our effective funding, we were again able to ensure affordable financing for our customers.

The legislative package for Finland’s long-prepared health and social services reform was largely completed in June, allowing municipalities to launch practical preparations. In the future, MuniFin’s customers will include the new wellbeing services counties.

Our customers play a key role in mitigating climate change and promoting the green transition. We support our customers in this transition by offering them green finance and sharing our expertise. In 2021, the demand for our green finance continued to grow, and the social finance that we launched in 2020 established its position among our customers.

MuniFin’s year started with a renewed organisation and was characterised by renewal and the rooting of new operating models. I wish to thank our customers for their close collaboration and our staff for their excellent work during this year of external and internal upheaval.

Information on Group results

Consolidated income statement

01–12/2021

01–12/2020

Change, %

(EUR million)

Net interest income

280

254

10.3

Other income

4

2

85.4

Income excluding unrealised fair value changes

285

257

11.0

Commission expenses

-5

-5

-0.2

Personnel expenses

-18

-18

-0.3

Other items in administrative expenses

-17

-15

11.6

Depreciation and impairment on tangible and intangible assets

-16

-6

>100

Other operating expenses

-16

-15

6.6

Costs

-72

-58

22.4

Credit loss and impairments on financial assets

0

-1

-87.8

Net operating profit excluding unrealised fair value changes

213

197

8.0

Unrealised fair value changes

27

-3

<-100

Net operating profit

240

194

23.5

Profit for the financial year

192

155

23.4

The sum of individual results may differ from the displayed total due rounding. Changes of more than 100% are shown as >100% or <-100%.

Group’s net operating profit excluding unrealised fair value changes

MuniFin Group’s core business operations remained strong during 2021. The Group’s net operating profit excluding unrealised fair value changes grew by 8.0% (6.2%) and totalled EUR 213 million (EUR 197 million). Income excluding unrealised fair value changes was EUR 285 million (EUR 257 million) and grew by 11.0% (4.3%). The Group’s costs were EUR 72 million (EUR 58 million) rising by 22.4% from the previous year. The non-recurring item related to impairment on on-going IT system implementation, EUR 10.5 million, increased costs. Costs excluding the non-recurring item grew as predicted and were 4.4% higher than in previous year (-3.0%). The COVID-19 pandemic did not have a significant negative impact on the Group’s core business and profitability in 2021 or in comparison year.

Net interest income totalled EUR 280 million (EUR 254 million), and increased by 10.3% (5.8%) from the previous year. Net interest income was positively affected by growing volumes and low market interest rates. In October 2021, the Group changed the conditions of its long-term customer loans with variable interest rates so that its customers will benefit from negative reference rates better than before. This change only had a minor effect on the Group’s profits. The Group’s net interest income does not recognise the interest expenses of EUR 16 million of the AT1 capital instrument, as the capital loan is treated as an equity instrument in the consolidated accounts. The interest expenses of the capital loan are treated similarly to dividend distribution; that is, as a decrease in retained earnings under equity upon realisation of interest payment on an annual basis.

Other income grew from the previous year to EUR 4 million (EUR 2 million). Other income includes commission income, realised net income from securities and foreign exchange transactions, net income on financial assets at fair value through other comprehensive income, and other operating income. In addition, the turnover of MuniFin’s subsidiary company Financial Advisory Services Inspira is included in the other income.

During 2020, the COVID-19 pandemic slowed cost growth, making the year’s costs unusually low. Costs started rising again in 2021, although the growth was slower than before the pandemic.

Commission expenses totalled EUR 5 million (EUR 5 million) and consisted primarily of paid guarantee fees, custody fees and funding programme update fees.

Administrative expenses reached EUR 35 million (EUR 33 million) and grew by 5.2% (2.3%). Of this, personnel expenses comprised EUR 18 million (EUR 18 million) and other administrative expenses EUR 17 million (EUR 15 million). Personnel expenses were almost at the same level than in previous year and were 0.3% (0.8%) less than in 2020. There were no significant changes in employee numbers and the average number of employees in the Group was 162 (167). Salary and pension costs decreased slightly during the financial year.

Other items in administrative expenses grew by 11.6% (4.0%) during the financial year. The cost of maintaining and developing information systems has increased IT expenses, but on the other hand, the COVID-19 pandemic has reduced certain types of expenditure, such as travelling expenses both in 2021 and 2020. In 2019, MuniFin Group signed outsourcing agreements for IT end-user and infrastructure services as well as the operation of the business IT systems to improve operational reliability and the availability of services. This implementation project was completed in late 2021.

During the financial year, depreciation and impairment of tangible and intangible assets reached EUR 16 million (EUR 6 million). The item includes impairment of EUR 10.5 million on the Group’s significant on-going IT system implementation.

Other operating expenses increased by 6.6% (-17.1%) to EUR 16 million (EUR 15 million). Fees collected by authorities increased by 23.0% (13.6%) to EUR 9 million (EUR 7 million), mainly due to an increase in the contribution to the Single Resolution Fund, which grew by 30.5% to EUR 6.7 million (EUR 5.2 million). These fees excluded, other expenses were EUR 6 million (EUR 7 million), decreasing by 10.3% (-35.1%), mostly due to smaller purchases of external services compared to 2020. Other expenses include a provision of EUR 0.4 million related to a possible tax increase following a tax interpretation issue from previous years.

The amount of expected credit losses (ECL), calculated according to IFRS 9, decreased during the financial year and was EUR -0.1 million (EUR -0.9 million). MuniFin Group has updated the scenarios and weights used to calculate ECL.

In 2020, MuniFin Group recorded an additional discretionary provision (management overlay) of EUR 0.3 million to take into account the financial effects of the COVID-19 pandemic. This was due to the fact that the deteriorating financial situation of certain customer segments had not yet reflected in MuniFin Group’s internal risk ratings for these segments, and therefore the Group’s management decided to record an additional discretionary provision based on a group-specific assessment. The financial situation of these customer segments later improved, and the management decided to remove the additional discretionary provision in late 2021. At the end of 2021, the Group’s management decided to record an additional discretionary provision of EUR 0.4 million to take into account ECL model changes that will take place in 2022. During 2022, the Group will further develop loss given default (LGD) calculation of mortgage loans as well as lifetime ECL calculations.

The Group’s overall credit risk position has remained low. According to the management’s assessment, all receivables will be recovered in full and no final credit loss will therefore arise, because the receivables are from Finnish municipalities, or they are accompanied by a securing municipal guarantee or a state deficiency guarantee supplementing mortgage collateral. During the Group’s history of more than 30 years, it has never recognised any final credit losses in its customer financing.

At the end 2021, the Group had a total of EUR 19 (EUR 24 million) of guarantee receivables from public sector entities due to customer insolvency, which are still under 0.01% of total customer exposure. The credit risk of the liquidity portfolio has remained at a good level, its average credit rating being AA+ (AA+).

Group’s profit and unrealised fair value changes

The Group’s net operating profit was EUR 240 million (EUR 194 million). Unrealised fair value changes improved the Group’s net operating profit by EUR 27 million, while in the previous year it had a negative impact of EUR 3 million. In 2021, net income from hedge accounting amounted to EUR 5 million (EUR 4 million) and unrealised net income from securities transactions to EUR 22 million (EUR -7 million).

The Group’s effective tax rate during the financial year was 20.1% (20.0%). Taxes in the consolidated income statement amounted to EUR 48 million (EUR 39 million). After taxes, the Group’s profit for the financial year was EUR 192 million (EUR 155 million). The Group’s full-year return on equity (ROE) was 10.7% (9.4%). Excluding unrealised fair value changes, the ROE was 9.6% (9.6%).

The Group’s other comprehensive income includes unrealised fair value changes of EUR -3 million (EUR -32 million). During the financial year, the most significant item affecting the other comprehensive income was cost-of-hedging, EUR -3 million (EUR -16 million). The fair value change due to changes in own credit risk of financial liabilities designated at fair value through profit or loss totalled EUR 0.4 million (EUR -17 million).

On the whole, unrealised fair value changes net of deferred tax affected the Group’s equity by EUR 19 million (EUR -28 million) and CET1 capital net of deferred tax in capital adequacy by EUR 19 million (EUR -15 million). The cumulative effect of unrealised fair value changes on the Group’s own funds in capital adequacy calculations was EUR 31 million (EUR 12 million).

Unrealised fair value changes reflect the temporary impact of market conditions on the valuation levels of financial instruments at the reporting time. The value changes may vary significantly from one reporting period to another, causing volatility in profit, equity and own funds in capital adequacy calculations. The effect on individual contracts will be removed by the end of the contract period.

In accordance with its risk management principles, MuniFin Group uses derivatives to financially hedge against interest rate, exchange rate and other market and price risks. Cash flows under agreements are hedged, but due to the generally used valuation methods, changes in fair value differ between the financial instrument and the respective hedging derivative. Changes in the shape of the interest rate curve and credit risk spreads in different currencies affect the valuations, which cause the fair values of hedged assets and liabilities and hedging instruments to behave in different ways. In practice, the changes in valuations are not realised on a cash basis because the Group primarily holds financial instruments and their hedging derivatives almost always until the maturity date. Changes in credit risk spreads are not expected to be materialised as credit losses for the Group, because the Group’s liquidity reserve has been invested in instruments with low credit risk. In the financial year, unrealised fair value changes were influenced in particular by changes in interest rate expectations and credit risk spreads in the Group’s main funding markets.

Parent Company’s result

MuniFin’s total net interest income at year-end was EUR 264 million (EUR 238 million), and its net operating profit stood at EUR 223 million (EUR 178 million). The profit after appropriations and taxes was EUR 137 million (EUR 22 million). The interest expenses of EUR 16 million for 2021 on the AT1 capital loan, which forms part of Additional Tier 1 capital in capital adequacy calculation, have been deducted in full from the Parent Company’s net interest income (EUR 16 million). In the Parent Company, the AT1 capital loan has been recorded under the balance sheet item Subordinated liabilities.

Subsidiary Inspira

The turnover of MuniFin’s subsidiary company, Financial Advisory Services Inspira Ltd, was EUR 1.7 million for 2021 (EUR 2.8 million), and its net operating profit amounted to EUR 0.1 million (EUR 0.1 million).

Outlook for 2022

According to the MuniFin Group’s current view, global economic growth is slowing down, but the main trend in the economic outlook remains still relatively positive. Employment continues to have room for growth, household savings lend support to consumption potential and private investments are expected to remain at a good level. The first half of the year will suffer from the uncertainty caused by the coronavirus Omicron variant. The high price of energy and the ongoing component shortage will continue to cause cost pressures and take their toll on economic activity. Economic forecasts continue to be highly uncertain.

The main trends in monetary policy are the same in the United States and Europe, but their central banks will move at a considerably different pace. The risk of the economy overheating in the United States is real, and the central bank Fed is likely to have to raise its key interest rates several times, already in 2022. In the euro area, the increased inflation is still mainly explained by reasons that are expected to be temporary. The ECB’s new symmetrical inflation target of 2% leaves the central bank more leeway to ignore temporary cost-push inflation. The ECB is likely to scale down its non-standard measures in 2022, but presumably very gradually. It now seems that a prudent normalisation of the interest rate policy could begin in late 2023, when the euro area should reach its pre-pandemic growth path. The outlook in monetary policy continues to be highly prone to changes in the pandemic situation.

In Finland, labour shortage and the increasing price of necessities will slow down economic growth in 2022. GDP growth will nevertheless remain somewhat stronger than Finland’s long-term growth potential. Unemployment is expected to fall below 7%.

The central government’s COVID-19 support package will no longer boost municipal finances in 2022, returning the focus on structural imbalances. More specific assessments of how the health and social services reform will impact individual municipalities will not be available until spring 2022. The reform’s practical challenges and the uncertainty of its financial impact make it difficult to predict municipal finances over the next few years.

In 2022, the health and social services reform will be reflected in the Group’s operations as practical preparation to act as a financing counterparty to the new wellbeing services counties. It is difficult to estimate the wider economic impact of the reform at this stage, when there is no practical information available on how wellbeing services counties will function. Wellbeing services counties’ future level of investments will effect on MuniFin’s financing volumes, but on the other hand the operating expenditures of the counties will be covered from the government’s budget. In MuniFin’s financing operations, health and social services lending plays such a role that changes in it will not have a material impact on MuniFin’s financial development in the near future.

After confirmation of its status as a public development credit institution, MuniFin decided in June 2021 to change the conditions of its long-term customer loans with variable interest rates in a way that will allow customers to benefit from negative reference rates better than before, which will clearly make the Group’s 2022 net interest income lower than in the previous year. The Group’s customer operations and funding are expected to continue to run and develop steadily. Operating expenses are expected to grow from 2021, as investments in IT systems and operational reliability as well as the marked rise in supervisory fees all increase expenses.

Considering the above-mentioned circumstances, the Group expects its net operating profit excluding unrealised fair value changes to be significantly lower than in the previous year, as per the Group’s long-term profitability targets and more beneficial customer pricing enabled by these targets. The Group expects its capital adequacy ratio and leverage ratio to remain very strong. The valuation principles set in the IFRS regulatory framework may cause significant but temporary unrealised fair value changes, some of which increase the volatility of net operating profit and make it more difficult to estimate in the short term.

These estimates are based on a current assessment of the development of MuniFin Group’s operations and the operating environment.

Webinar for investors and other stakeholders

MuniFin Group’s results for the year 2021 will be presented to investors and other stakeholders in a results webinar held on 9 February 2022 at 2:00 pm EET. Register for the webinar here. Register here if you are not able to attend but wish to receive a recording.

Municipality Finance Plc

Further information:

Esa Kallio, President and CEO, tel. +358 50 337 7953

MuniFin (Municipality Finance Plc) is one of Finland’s largest credit institutions. The company is owned by Finnish municipalities, the public sector pension fund Keva and the Republic of Finland. MuniFin Group also includes the subsidiary company, Financial Advisory Services Inspira Ltd. The Group’s balance sheet is over EUR 46 billion.

MuniFin builds a better and more sustainable future with its customers. MuniFin’s customers are Finnish municipalities, municipal federations, municipally controlled entities and non-profit housing organisations. Lending is used for environmentally and socially responsible investment targets such as public transportation, hospitals and healthcare centres, schools and day care centres, and homes for people with special needs.

MuniFin’s customers are domestic but the company operates in a completely global business environment. The company is an active Finnish bond issuer in international capital markets and the first Finnish green and social bond issuer. The funding is exclusively guaranteed by the Municipal Guarantee Board.