MuniFin Group maintained steady operations in the first half of 2024 despite the challenges in the operating environment.

The Group’s net operating profit excluding unrealised fair value changes amounted to EUR 89 million, growing from the comparison period and exceeding the previous year’s figure by 9.6%. The increase in net operating profit was boosted mostly by rising short-term market rates and lower expenses than in the comparison period.

New long-term customer financing increased in January–June and amounted to EUR 2.4 billion. Long-term customer financing (long-term loans and leased assets) excluding unrealised fair value changes totalled EUR 34.3 billion at the end of June and saw an increase of 4.0% in the reporting period. The total amount of green finance aimed at environmentally sustainable investments and social finance aimed at investments promoting equality and communality increased by 15.7% during the reporting period. The ratio of green and social finance to long-term customer financing excluding unrealised fair value changes grew to 23.7%.

In January–June, new long-term funding reached EUR 4.9 billion. At the end of June, the total funding was EUR 44.5 billion. The Group’s total liquidity is very strong. The Group’s leverage ratio also remained at a strong level, standing at 12.0% at the end of June. At the end of June, the Group’s CET1 capital ratio was very strong at 102.4%.

“The first half of 2024 was marked by continued economic uncertainty and inflation concerns. The challenges in the operating environment did not affect MuniFin’s performance, and we were able to successfully carry out our core mandate of ensuring the availability of affordable financing for our customers. In the first half of the year, municipalities had slightly lower demand for financing than expected, whereas the affordable social housing sector had high financing needs”, notes Esa Kallio, President and CEO at MuniFin.

The Group also published a separate Pillar III report on risk management and capital adequacy.

Read and download the Half Year Report

Our half year report for January–June 2024 can be read and downloaded in the reports and publications section of our website.

Pessi, a housing service unit located in Helsinki’s Vallila district, provides 125 apartments for people with a history of substance abuse or mental health problems. After comprehensive renovation, the building can now accommodate more people who have experienced prolonged homelessness.

Blue Ribbon Ltd, a part of the Finnish non-profit Blue Ribbon Foundation Group, offers supported housing for unhoused people who suffer from substance abuse or mental health issues. Their largest housing service unit Pessi went through a massive renovation that was finalized in 2023. The parent foundation’s administration, whose office was in the same building, moved away to make space for 27 new apartments.

“Finding apartments for this customer group has proved extremely challenging. As a solution, we built more apartments to a property where we already have other people in a similar situation and services in place,” says Elli Korte-Lilja, Real Estate Manager at Blue Ribbon Foundation.

The renovation, which was financed through MuniFin’s social finance, added to both the building’s security and coziness. A new accessible 16-apartment unit was also built in the renovation process.

“For a long time, we have struggled with not being able to house people with mobility impairments at Pessi. Normally these people would resort to service housing or intensive service housing, but they aren’t allowed in due to a history of substance abuse. We had to build more apartments so that these people could get the support and help they need,” Business Director of Blue Ribbon, Sanni Joutsenlahti, explains.

Housing is a basic right, not a reward

According to 2023 data from Ara (The Housing Finance and Development Centre of Finland), there are approximately 1,000 long-term homeless individuals in Finland. Ara based their data on information gathered from municipalities. Numbers are not available from all municipalities, which means that the actual number of long-term homeless people could be somewhat higher. A person is considered long-term homeless if they have been unhoused for at least one year or repeatedly over the last three years.

Blue Ribbon Foundation helps the most vulnerable and works to end homelessness. Blue Ribbon Ltd, belonging to the same group, provides supported housing according to the Housing First principle. This means that a permanent home is not viewed as a reward that needs to be earned through sobriety, but a home in itself is the first step on the road to recovery. Thanks to the Housing First model, Finland has been successful in reducing homelessness.

“The idea is that you can come live with us first; only then do we start thinking about your individual rehabilitation. When a person has a home and a place to rest their head, their circumstances in life also tend to calm down,” Sanni Joutsenlahti says.

Pessi residents have their own counselors to support them in rehabilitation and daily errands. Everything starts from the basics: first, the residents practice daily rhythms and regular mealtimes. Many residents need help with everyday chores, such as boiling potatoes, cleaning, or managing their own finances.

Finding your footing through community and action

Although the residents face various issues in their everyday lives, in many ways Pessi resembles any other housing association. In their weekly community meetings, the residents may discuss their communal sauna facilities, the draft coming through the windows, or other very similar matters to those discussed in countless other tenant meetings across the country.

The employees and residents form a tight-knit community that organizes plenty of joint activities, ranging from courtyard concerts to movie screenings and music groups. The residents are also offered peer groups that support rehabilitation.

Sanni Joutsenlahti has been thrilled about seeing how work has the capacity to help people. The building’s residents are offered opportunities to try their hand at various forms of employment and training.

“When offered this personal agency, people get to experience moments where they feel they are good at something. We have a lot of professionals living here, such as painters and electricians, and employment helps them get back on their feet. Many people start by doing small activities around the house. After noticing that they have the skills and energy to work, they may move on to rehabilitative work or work trials,” Joutsenlahti says.

“For someone, making oatmeal for the whole crew every Wednesday morning can be the most important thing in the world.”

Affordable social housing

The Finnish affordable social housing sector plays a significant role in the development of a sustainable welfare state. In Finland, affordable social housing is mainly provided by municipality-owned companies and nationwide non-profit organisations. MuniFin is the main financier of affordable social housing production in Finland. An increasing amount of housing in Finland is being constructed and financed with consideration for social and environmental factors.

Niiralan Kulma, the largest rental company in Kuopio, invests significantly in sustainable and environmentally friendly living.

Niiralan Kulma’s recent investments adapt to the changing needs of Kuopio. New residents move to the city for work, and they need comfortable homes. Simultaneously Kuopio is preparing for population ageing by building service housing.

“Ten years ago, we talked about affordable, quality housing. Now our strategy has expanded to include responsibility, which must cover environmental and social values,” says Kari Keränen, CEO of Niiralan Kulma.

Seven new apartment buildings are currently financed with MuniFin’s green finance, and three service housing projects have been completed with MuniFin’s social finance.

“When we evaluated long-term interest rates, MuniFin offered the most affordable solution. The margin and the interest rate were lowered because these new projects are green and social.”

Cozy and environmentally friendly homes

Niiralan Kulma is building homes in seven different locations across the city of Kuopio.

“We are planning and building cozy homes that effectively utilise energy-saving technology and renewable energy. Building technology takes into account the by-products of energy. We use geothermal heat, recover heat from wastewater, capture excess energy from mechanical ventilation, and utilise solar energy. It was very important to design the houses to be maintenance-free and long-lasting,” Keränen says.

Many methods are in use to improve environmental friendliness. The new apartments do not have unusable space that requires heating, and there are multiple waste bins in the apartments for recycling.

“In addition to the living spaces, we have invested in bicycle parking and charging points for electric cars. The smallest details are important, for example, with electronic notice boards, no papers have to be printed to inform the residents.”

Service housing for seniors and young adults

Männistön Aimu, which offers rehabilitative service housing for young adults, was completed in early 2020. Next completed in 2022, Liito-orava care home, provides service housing apartments and rental apartments for seniors. Most recently, Levänen service center was opened for residents in October 2023.

“Both the service center and the care home offer 60 places for residents, which are rented by the wellbeing services county of North Savo. They also organise the care needed by seniors.”

Residents were involved in the planning of the service centers, and they as well as the care staff have been satisfied with the end results. Männistön Aimu’s small apartment building is inviting from the outside: unpainted wooden surfaces of the house are environmentally friendly and stand out from the street view.

The costs of these projects were the following: Männistön Aimu is EUR 2.1 million, Liito-orava is EUR 10.2 million and the Levänen service center is EUR 8.7 million.

“We want to thank the staff of MuniFin. We received a lot of help and clear instructions when we needed them. The financing arrangement has been smooth.”

Affordable social housing

The Finnish affordable social housing sector plays a significant role in the development of a sustainable welfare state. In Finland, affordable social housing is mainly provided by municipality-owned companies and nationwide non-profit organisations. MuniFin is the main financier of affordable social housing production in Finland. An increasing amount of housing in Finland is being constructed and financed with consideration for social and environmental factors.

The City of Kokkola won our Green Pioneer of the Year competition last year. The prize money was used to organize a competition in which local children and youth could propose ideas for sustainable development initiatives.

Last fall, MuniFin awarded Kokkola the Green Pioneer of the Year title. The competition prize was EUR 10,000, which the winner could use for a sustainability project of their choice.

With the prize money, Kokkola organized a competition where preschool and school children could innovate projects related to climate and the environment.

“Environmental issues are crucial for the happiness of the younger generation. That’s why we in Kokkola believe in our children and young people and wanted to involve them in brainstorming for a green future,” explained Veli-Matti Isoaho, Head of Construction for the City of Kokkola, on the decision to organize the competition.

A total of 44 teams participated in the competition in four different age categories. Each team could submit one project for the competition. Ideas were collected during February and March 2024.

Ambitious and creative projects impressed the jury

The winners of the competition were announced at an award ceremony in early May organized by the City of Kokkola. The following groups were selected for their innovative ideas:

Early Childhood Education

Winner: Ulkometsä Daycare

Project: Integrating Recycling into Daily Daycare Activities

Preschool – 2nd Grade

Winner: Lohtaja Kirkonkylä School, 2nd Grade

Project: Nature-Friendly Schoolyard

3rd – 6th Grade

Winner: Kälviä Marttila School, 6th Grade

Project: Marttila School’s Backyard Garden

Junior High

Winner: Hakalahti School, 9A

Project: Biodiversity Protection Campaign

Each category winner will receive an EUR 2,500 cash prize, which the class or group can use as they wish.

Green Pioneer of the Year Won with the Piispanmäki Project

Last year, Kokkola won the competition with the Piispanmäki multi-functional building project. The city’s commitment to green financing requirements impressed the competition’s evaluation panel.

“Kokkola has admirably taken ownership of sustainable construction, which was evident in the Piispanmäki project. The initiative was managed internally, with the entire organization committed to it. It was a pleasure to see how Kokkola’s children and young people were involved in environmental discussions,” said Daniel Eriksson, MuniFin’s Customer Relationship Manager.

MuniFin first named a Green Pioneer of the Year among its clients in 2019, recognizing those who have ambitiously advanced climate and environmental goals.

In 2023, the number of our social finance projects increased by over 40% from the year before. A growing awareness of sustainability matters coupled with increasing stakeholder expectations are pushing up the demand for our sustainable finance.

Our raison d’être and the main duty of our customers is to build up the Finnish welfare state. Our customers are tasked with organising the basic functions of society, such as health and social services, daycare, basic education, care for the elderly, infrastructure, affordable housing and various cultural and sports services. The values of the Nordic welfare state are inherent in the work of our social finance customers, whose investments often also benefit the environment and climate.

We published our first sustainability agenda in October, sharing our goal of increasing the proportion of our social finance to 8% of our long-term customer financing by 2030. More and more, our customers are bringing up themes related to our social and green finance in our interactions, signalling a growing awareness of sustainability. Our customers’ own stakeholders are also interested in these themes, so the push to improve sustainability is coming from many fronts. As a result, a growing number of projects are now meeting the criteria for our sustainable finance.

In 2023, the number of projects accepted into our social finance portfolio increased by over 40% from the year before. We approved 34 projects, the majority of which are welfare projects or housing solutions aimed at the most vulnerable population. It is safe to say that we are well on the way towards our goal.

The responsibility for organising healthcare, social welfare and rescue services was transferred from municipalities to wellbeing services counties on 1 January 2023, but municipalities nevertheless continue to play a vital role in promoting good health and wellbeing. Many of our social finance projects are important not only to their users, but also to the vitality of the municipality. Investments that generate activity are a signal to companies that the municipality will stay vital.

For residents, social finance projects signify better services: communal living solutions, healthcare services, modern and healthy learning environments and more opportunities for hobbies, cultural activities and sports. In addition to creating the setting for municipal operations, the project buildings often double as venues for sports, culture and other activities offered by the voluntary sector. The projects cater for people of different ages, backgrounds and cultures, but most of all, they bring people together. This is the social glue that we need to keep the welfare society together in a time of heightened individualism and polarisation.

Rami Erkkilä, Senior Specialist, sustainable finance Rami Erkkilä is responsible for green and social finance products at MuniFin.

The article was originally published on the 7th of March as a part of MuniFin Social impact report 2023.

The Finnish affordable social housing sector plays a significant role in the development of a sustainable welfare state. In 2023, a vast majority of MuniFin’s housing loans were granted to either green or social finance projects.

An increasing amount of housing in Finland is being constructed and financed with consideration for social and environmental factors. Our customers, including affordable social housing organizations and municipal rental housing projects, play a significant role in this trend. Last year, the share of green and social finance in our housing loans reached a record high of 63 percent.

“An increasing number of our customers have made it their mission to carry out their projects more sustainably, taking into account environmental, climate or social benefits. Affordable social housing production is at the absolute forefront of sustainable construction in Finland”, says Päivi Petäjäniemi, Customer Relations Manager at MuniFin.

MuniFin was the first in Finland to start offering green finance for climate and environmentally friendly projects in 2016. In 2020, we also became the first to launch social finance, which emphasizes the social benefits of the projects: equality, communality, safety, welfare, or regional vitality.

“Our customers were among the first to learn about green and social finance, and we have persistently kept the topic on the agenda ever since. Nowadays, they have comprehensive knowledge of their alternatives, and they proactively seek green and social finance to give visibility to their projects. All their projects are significant for the Finnish welfare society, but the ones that fall under the green and social finance framework, are truly best in class”, Petäjäniemi explains.

Buildings and construction account for about a third of Finland’s greenhouse gas emissions*. The figures show that Finnish municipalities and non-profit housing operators are strongly involved in climate efforts.

The energy efficiency of affordable social housing buildings is generally higher than buildings in the private sector*. One factor is the forthcoming Corporate Sustainability Reporting Directive (CSDR), which is already directing the larger operators towards more sustainable choices. Also, the residents of newly constructed homes are increasingly demanding more energy-efficient housing solutions.

“More and more buildings are built in energy class A, which is the minimum demand in our green finance framework. Our customers are bold and want to try new things, so I expect to see a rising number of projects that also consider the impacts of the entire life cycle and construction chain. The challenge for now is that costs may seem higher in the construction phase. Saved energy costs for example, show in the long run, and our customers have strict demands for affordability from The Housing Finance and Development Centre of Finland (Ara), which oversees the projects.”

The prerequisites for the approval of social finance projects consider the social benefits of the projects.

“Our customers are increasingly planning housing as a whole, and this is clearly visible in projects for special groups. For example, they want to provide every student with their own apartment, but there is increasing investment in shared spaces, which promotes community and prevents loneliness. Residents are also offered various services, such as car-sharing or resident counselling”, Petäjäniemi says.

Finnish affordable social housing supports social mixing and brings down homelessness

In Finland, affordable social housing is mainly provided by municipality-owned companies and nationwide non-profit organisations. The production is financed through interest subsidy loans. The loans are guaranteed by the Finnish state through The Housing Finance and Development Centre of Finland (Ara), which is administered by the Ministry of the Environment. Alternatively, housing projects can also be loans to municipality owned companies. These loans do not have a state interest subsidy, but they come with a 100% municipal guarantee.

MuniFin is the main financier of affordable social housing production in Finland. The loan periods are long, up to 41 years.

The Finnish government updated its housing policy development programme in 2021. Some of the main objectives of this programme include increasing housing construction in growing urban areas and eradicating homelessness within two government terms. Affordable social housing has played a remarkable role in tackling homelessness in Finland, especially family homelessness. Affordable social housing is also instrumental in preventing segregation and facilitating labour mobility.

Our sustainability agenda sets the direction until 2035

As outlined in our strategy, key aspects of sustainability at MuniFin include acting as our customers’ partner in building a sustainable society while efficiently managing climate-related and environmental risks.

Our long-term impact stems from the products and services we offer our customers. In our sustainability agenda published in 2023, we set the direction and goals for our sustainability efforts until 2035.

In this agenda, we commit to increasing the proportion of sustainable finance in our lending portfolio into one third by 2030. In 2023, the share was 21,3 percent. We also set emission reduction targets for financed buildings. Our target level is 8 kgCO₂/m² by 2035, representing reduction compared to the 2022 level.

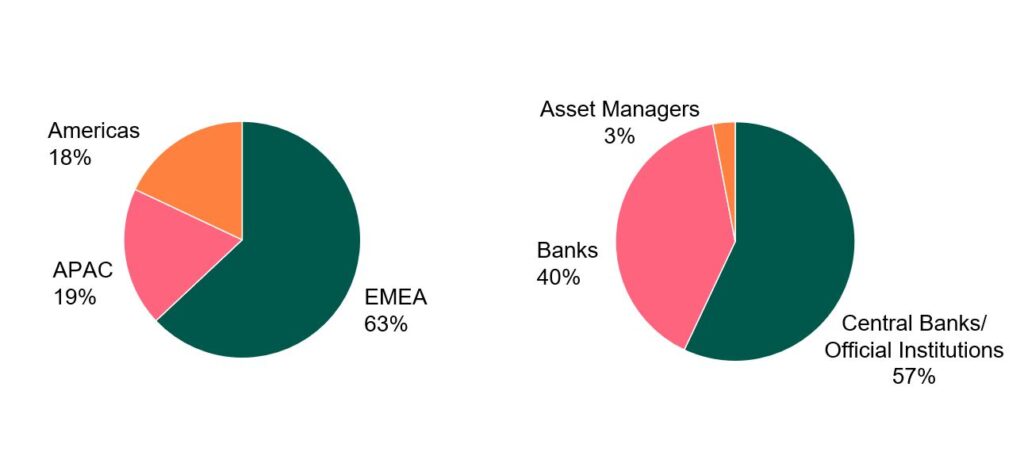

Three months following the record-breaking USD 1.5 billion issuance in January, MuniFin returns to the USD market with another 1 billion benchmark. The 3-year bond successfully gathered a high-quality orderbook.

On Tuesday 16 April, MuniFin issued a new 3-year USD 1 billion benchmark with initial price guidance of MS+33 basis points. Investor demand continued to grow throughout the morning and books closed a few hours later in excess of USD 1.5 billion.

The bond was priced at MS +33 basis points, consistent with the initial guidance, with a coupon of 4.875%, a reoffer price of 99.708% and a re-offer yield of 4.981%. It carries a spread of 18 basis points over the CT 3 4.500% due 15 April 2027.

The final orderbook was geographically diverse with 48 high-quality accounts participating. Central banks took 57% of the allocations, followed by Banks and bank treasuries (40%), and Asset Managers, taking the remaining 3%.

“Investor demand started to accumulate after a moderate start, eventually reaching over USD 1.5 billion. We were particularly pleased with the quality of the final orderbook, as majority was allocated to central banks and official institutions. We have now successfully secured a little less than half of our funding target for the year”, says Analyst Aaro Koski.

After this transaction, MuniFin has now completed EUR 4.5 billion of its EUR 9–10 billion funding programme for 2024.

Aaro Koski, Analyst at MuniFin’s Funding and Sustainability team.

Distribution

Transaction details

Issuer:

Municipality Finance Plc (“MuniFin”)

Rating:

Aa1 / AA+ (Moody’s/S&P – both stable)

Issue Size:

USD 1 billion

Payment Date:

23 April 2024 (T+5)

Maturity Date:

23 April 2027

Coupon:

4.875%

Re-offer Price:

99.667%

Re-offer Yield:

4.996%

Re-offer vs. Mid Swaps:

+33bps

Re-offer vs. Benchmark:

CT 3 4.500% due 15 April 2027 +18bps

ISIN:

XS2807531657 / US62630CEL19

Lead Managers

J.P. Morgan SE, Morgan Stanley Co & International PLC, Nomura Financial Products Europe GmbH, TD Global Finance unlimited company

Comments from Lead Managers

Ben Adubi, Managing Director, Head of SSA, Morgan Stanley:

“Another successful outing in the USD market for MuniFin following their strong 5-year issued earlier this year. Taking advantage of the favourable move in swap spreads and recent sell-off in rates, the deal amassed a high-quality and granular orderbook with 57% of allocations to CB/OIs, which is a testament to the strength of MuniFin’s credit quality and their opportunistic funding strategy. Congratulations to the MuniFin team on a stellar start to Q2, following on from an impressive start to the year, Morgan Stanley is delighted to have been involved!”

Mark Yeomans, Managing Director, Nomura:

“Yet another strong USD outing from MuniFin; with the new 3-year benchmark complementing the 5-year issued earlier in January. MuniFin took advantage of the global back up in rates to deliver another record 4.875% coupon for investors, as witnessed in their previous 3-year from last October. The quality of the orderbook is a testament to the investor following that MuniFin enjoys as a safe haven asset and the diligent investor outreach of the entire funding team. Nomura were delighted to be a part of such an important transaction.”

Ioannis Rallis, Executive Director, Head of SSA DCM, J.P. Morgan:

“Congratulations to the MuniFin team for printing another solid USD benchmark this year! Despite uncertain geopolitical backdrop and busy pipeline in the week, MuniFin was successfully able to achieve its tightest spread vs SOFR MS (+33bps) for a MuniFin USD 3-year benchmark. The high quality of the orderbook reflected in the 57% allocation to CB/OIs is a testament to investor confidence in MuniFin’s name. We are delighted to be involved in this transaction.”

Laura Quinn, Managing Director, Global Co-Head of SSA and Head of Dublin Debt Capital Markets:

“Congratulations to the MuniFin team on a successful USD benchmark transaction, launching their first 3-year USD benchmark in 2024 and second USD benchmark this year. MuniFin secured an efficient funding window this week to ensure they could complete their USD 1 billion funding exercise. The exceptionally high-quality orderbook is a testament to MuniFin’s standing in the fixed income market.”

MuniFin is part of a Nordic public sector issuer group that has released a new edition of the Position Paper on Green Bonds Impact Reporting. The updates to these reporting recommendations stem from recent market developments, especially from emission reductions in energy production.

Published by Nordic public sector issuers, the Position Paper on Green Bonds Impact Reporting is a practical guide to reporting the environmental impact of projects financed through green bonds. It includes impact indicators, calculation methods and reporting practices.

“The material changes in the 2024 update include revised emission factors for electricity and district heating, new recommendations for vintage reporting and more specific recommendations on topics such as look-back/allocation periods, refinancing, ESG strategy and risk management”, says MuniFin’s Sustainability Manager Mikko Noronen.

In the latest edition of the position paper, the issuer group revised the emission factors for electricity and district heating downwards to reflect the energy sector’s rapid transition towards fossil-free energy sources.

Nordic recommendations harmonise the green bonds market

The purpose of the Nordic reporting recommendations is to create harmonious and transparent green bonds impact reporting principles that cultivate market practices. This allows issuers to report on the environmental impact of their financed projects in a way that offers investors high-quality information that is comparable, transparent and also supports the investors’ own reporting.

“For sustainable bonds to retain and strengthen their credibility as useful tools to finance the transition, it is of importance that market participants undertake issuance and reporting in a diligent and transparent manner”, says Björn Bergstrand, Head of Sustainability at Sweden’s Kommuninvest and coordinator of the Nordic cooperation.

Developed to assist Nordic public sector borrowers in reporting the environmental impact from their investments, the Position Paper on Green Bonds Impact Reporting has come to be used by issuers also in the private sector.

The Position Paper on Green Bonds Impact Reporting was first introduced in 2017 and is now in its fourth edition.

The Nordic public sector issuer group publishing the Position Paper on Green Bonds Impact Reporting includes MuniFin and MuniFin’s Nordic public sector counterparts, Kommunalbanken in Norway, KommuneKredit in Denmark and Kommuninvest in Sweden, as well as the Swedish Export Credit Corporation (SEK) and a number of Swedish municipal and regional issuers.

We have published our annual report for 2023. We have also published the impact reports on our green and social finance and the Pillar III disclosure report on capital adequacy.

The year 2023 was the fourth consecutive year marked by instability. In these uncertain times, our role as our customers’ trusted financing partner has grown even more important. At MuniFin, 2023 was a year when we put sustainability even more front and centre as we revised our strategy and published our first sustainability agenda.

The volatile operating environment did not significantly affect our performance. Our operations remained stable, and we were again able to successfully carry out our core mandate of providing affordable long-term financing for our customers.

Our long-term customer finance increased by about 10% from the previous year. Our new long-term customer financing remained on a par with 2022, totalling EUR 4.4 billion. Our profitability was slightly higher than in 2022.

The amount of our sustainable finance, i.e. our green and social finance, grew by about EUR 2 billion in 2023. Our sustainable finance products are our way of encouraging our customers to make more responsible investments. Read more about the impacts of our sustainable finance in the green and social impact reports published today.

What was the year 2023 like at MuniFin?

Oops! This video will not be shown because you have disabled the marketing cookies. To see the video, accept marketing cookies.

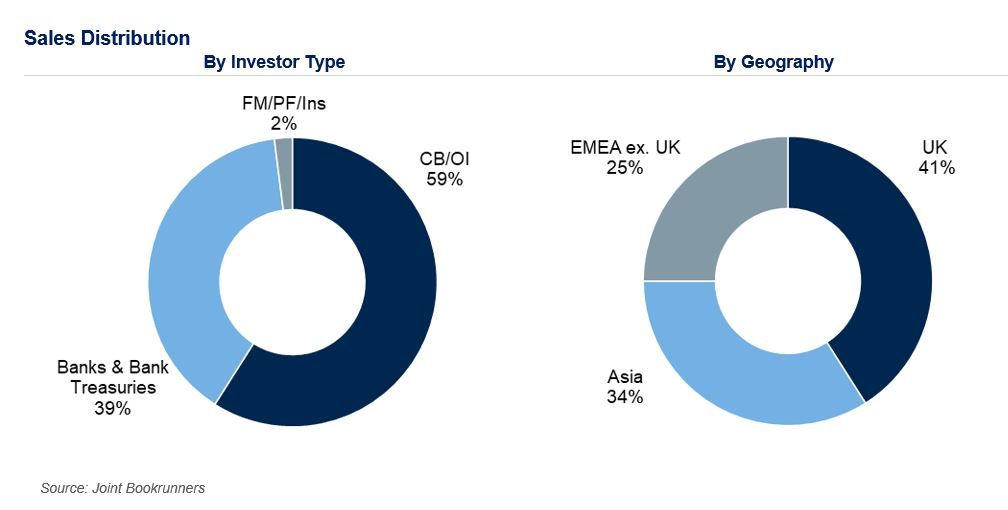

MuniFin’s GBP 250 million issue on February 29 was well received in the market, with particularly strong participation from central banks and official institutions. With this transaction, MuniFin has now printed one third of its EUR 9–10 billion funding programme for the year 2024.

Distribution of the transaction was once again broad both in terms of investor types and geographics, which is testament to MuniFin’s strong position in the global investor community.

Central banks and official institutions were the largest investor component, taking 59% of the final book. The participation was also strong from banks and bank treasuries (39%), with fund managers, pension funds and insurance accounts representing 2%. In terms of geography, the transaction was broadly diversified across UK (41%), Asia (34%) and EMEA ex. UK (25%) investors.

“This was our first GBP line of the year, and it was great to extend our GBP issuance curve today. We are grateful for the investor following we have in the Sterling market and it has been a pleasure to be able to be on the screens again”, says Senior Manager Karoliina Kajova from MuniFin’s funding and sustainability team.

“Congratulations to the MuniFin team for a strong return to the GBP market, taking advantage of a clear issuance window to extend their GBP curve with a new benchmark. The strong support from a diverse group of investors and the competitive price point is a testament to MuniFin’s standing in the international market. We’re delighted to be involved!” Tina Nguyen, Vice President, SSA DCM, J.P. Morgan

“Congratulations to the MuniFin team on the new GBP Oct-28 Benchmark. Taking advantage of a clear issuance window, MuniFin were able to extend their GBP Benchmark curve and maintain their regular presence in the Sterling SSA market. RBC were delighted to be a part of the transaction.” James Taunton, Director, SSA DCM, RBC Capital Markets

“We are delighted to be involved in MuniFin’s successful return to the Sterling market with their first GBP Benchmark of the year. This syndication is a clear demonstration of their global support from a diversified investor base. Congratulations to the MuniFin team on an excellent trade.” Paul Eustace, Managing Director, Global Co-Head of SSA and Head of Europe and Asia Syndicate, TD Securities

Further information

Joakim Holmström Executive Vice President, Capital Markets and Sustainability +358 50 4443 638

Antti Kontio Head of Funding and Sustainability +358 50 3700 285