Based on the latest annual review of recognised agencies in the Eurosystem collateral framework, MuniFin complies with the quantitative criteria of the European Central Bank as of 10 December 2021. In practice, this has decreased the haircuts applicable to bonds issued by MuniFin when they are used as collateral for Eurosystem credit operations. The decrease in haircuts amounts to approximately 5-12 percentage points, depending on the remaining maturity and the coupon structure (fixed, floating, zero coupon) of the bond. The change in haircuts became effective on Monday 13 December 2021.

For further information on the current valuation haircut levels applied to eligible marketable assets, please refer to the ECB Guideline ECB/2015/35 (as amended). MuniFin’s Eurosystem eligible bonds are allocated in Haircut Category II. Previously MuniFin’s bonds were allocated in Category IV.

MuniFin will continue to focus on issuing strategic benchmark bonds, which at MuniFin means EUR and USD denominated benchmarks. The plan is to issue approximately 2/3 of the funding through these EUR and USD strategic benchmark bonds and the rest 1/3 through tactical bonds, which at MuniFin equals other public markets (e.g. GBP, NOK, AUD), private placements and structured retail bonds in Japan. MuniFin plans to issue a public SOFR line in 2022, subject to market conditions.

MuniFin also aims to continue its commitment to issue in green and social bonds like in past years. We forecast to issue one green and one social bond in 2022. The sizes of the green and social bond issues will depend on the underlying asset development of the customer financing portfolio.

In 2021, MuniFin has thus far issued EUR 9.4 billion of new long-term funding. Approximately 50% was issued in strategic benchmark bond format in EUR and USD. This included two new 7- and 10-year EUR benchmarks and two new long 5-year USD benchmarks. MuniFin also tapped its EUR social bond maturing in 2035 by 500 million and issued a new green bond in GBP, MuniFin’s first green bond in the Sterling market.

The top 5 issuance currencies in 2021 are thus far EUR (37%), USD (26%), GBP (15%), JPY (14%) and NOK (5%). These currencies account for 97% of the new funding issued in 2021.

Further information

Antti Kontio Head of Funding and Sustainability, MuniFin Tel. +358 500 3700285

Structured notes are an important tool for MuniFin to diversify funding and cater the preferences of a broader investor base. Despite the structured note market shrinking considerably each year, MuniFin has been able to keep a strong presence.

– We have held a commitment to the market. In addition to our credit rating, we believe our success is due to our ability to adapt to new market trends. We strive to have an active dialogue with our dealer banks and investors, says Senior Manager Karoliina Kajova from MuniFin’s Funding and Sustainability team.

In 2021, the structured notes issuance volume has reached EUR 1,9 billion, which is 20% of total new funding.

– The percentage of structured funding has remained stable during the past few years. We continue to invest in risk modelling, which allows us to keep an active presence in the market also in the future, Kajova says.

MuniFin won the award also last year and three times in a row in 2016, 2017 and 2018.

CMD Portal is an independent collaborative market data network for bond and money market professionals. They provide access to a robust dataset, flexible data analysis tools and research on fixed income products for institutional asset managers, issuers and intermediaries.

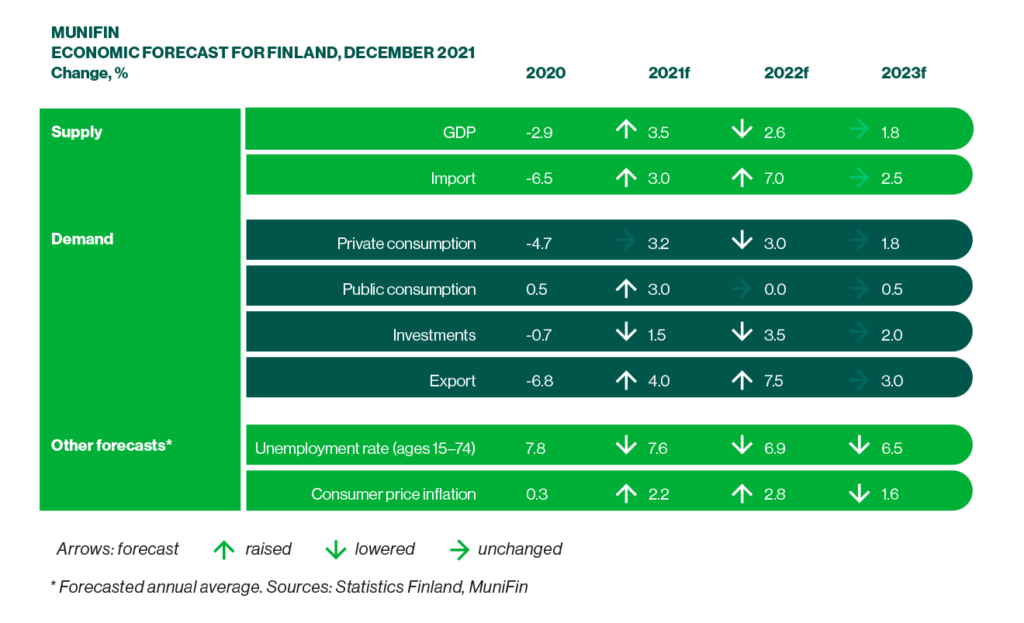

MuniFin’s fourth and final economic forecast for this year comes out at an exceptional time, says MuniFin’s Chief Economist Timo Vesala. The world economy continues to grow, but short-term risks are on the rise. Omicron, the new coronavirus variant discovered in South Africa, is raising uncertainty to a new level. Because very little is yet known about how dangerous the new variant is, how easily it spreads and how effectively vaccines protect against it, it is difficult to estimate what impact it will have on the economy.

“Our forecast accounts for the recent aggravation of the COVID pandemic, but not for the potential effects of the new variant. If vaccine efficacy proves significantly lower for Omicron than for the other variants, tighter restrictions may have to be imposed. This would also mean that economic recovery will be knocked off track”, explains Vesala.

Another current risk involves China, whose overheated property market is cooling down quickly. Construction investments have played an exceptionally large role in China’s economic growth.

“If China’s economic growth slows down considerably, this will affect the world economy as well”, Vesala assesses.

The business environment is also hampered by the increase of costs. Rising inflation weakens the buying power of consumers and thus also takes its toll on economic activity.

Long-term growth path Finland’s greatest problem

By international comparison, Finland has so far survived the pandemic with only a moderate effect on the economy. Finland’s GDP exceeded the pre-pandemic level already in the second quarter of this year. Employment has also recovered briskly, with the total number of people in employment reaching an all-time high this year.

As economic growth has exceeded expectations, MuniFin revised its growth forecast for this year, raising it from 3.2% to 3.5%. Due to increasing COVID uncertainty and rising costs, however, MuniFin lowered next year’s GDP growth forecast from 3.0% to 2.6%. MuniFin’s growth forecast for 2023 remains at 1.8%, which is slightly above Finland’s long-term growth potential.

According to Vesala, the biggest problem in the Finnish economy is that its long-term growth path is not sufficient to sustain the current welfare state. Finland should gradually start shifting the focus back from COVID damage control to bold economic reform.

“We must create an outlook in which companies have ready access to human capital. Otherwise, our economy will struggle to attract growth investments. To succeed, we must invest in education, research and attracting foreign workers. We should also be in the vanguard of the green transition”, summarises Vesala.

Fed expected to raise interests next year, Europe to follow later

Inflation has accelerated significantly in the autumn. The basic trends in monetary policy are the same in the United States and in Europe, but the central banks are moving at a different pace. The risk of the economy overheating is greater in the US.

“Unless the aggravating pandemic situation causes the short-term outlook to take a significant turn for the worse, the Fed is likely to raise its key interest rates as early as next year”, predicts Vesala.

Inflation uncertainty has also increased considerably in the euro area. Vesala nevertheless believes that the underlying factors, such as the spiking energy prices and disrupted supply chains, are mostly temporary.

“As the worst bottlenecks are being released, their price-increasing effects may be replaced by pressure to decrease prices, returning inflation below the ECB’s target level. The ECB’s new inflation target leaves the central bank more leeway to delay interest rate increases, and I think the ECB will use it.”

Vesala believes that the ECB will reduce its non-standard monetary policy measures in 2022. The time to gradually start normalising interest policy could be in late 2023.

Municipalities have enjoyed generous COVID support measures, which are now coming to an end

Almost all of the key indicators of municipal finances are now looking better than pre-pandemic forecasts expected. The central government has shouldered the main responsibility for mitigating the negative economic impact of the pandemic, ensuring that municipalities will not feel the pandemic pinch.

During COVID, the central government has taken on more debt, however going forward this calls for a stabilisation of the central government debt ratio.

“Generous COVID support measures are inevitably coming to an end”, predicts MuniFin’s CEO Esa Kallio.

The predictability of municipal finances is further complicated by Finland’s ongoing health and social services reform, which will transform the financing structure of municipalities. Municipalities with a strong tax base will lose proportionately more tax revenue than municipalities with a weak tax base. Kallio describes the outcome as unfavourable.

“After the reform, municipalities that can now rely on a growing tax income will become increasingly dependent on central government income transfers. And municipalities with a weakening tax base will increase their reliance on their own tax income. In both cases, a secure source of income is replaced by a more unreliable one.”

The health and social services reform also calls for the evaluation of the long-term prerequisites for growth. The level of education among young people is declining, and Finland has fallen below the OECD average in the percentage of tertiary graduates. Even after the social services reform is implemented, the provision of education will largely be the responsibility of municipalities. In many municipalities, a low birth rate is causing a shortage of pupils and pushing up the unit cost in education.

“With the health and social services reform halving municipalities duties and finances, there is a risk that education will take the hit and suffer the adjustments. Municipalities need more resources, but as of yet, it is unclear where these resources will come from”, Kallio says.

The platform is an electronic issuance and communication platform for the global debt capital markets, which enables communication between the issuer and dealers. Documentation and even contract signing are handled through the platform.

– Our pilot transaction went even smoother than expected, says Manager Miia Palviainen from MuniFin’s Funding and Sustainability team.

The pilot 1-year fixed rate bond in question was RON denominated and Citigroup Global Markets Europe acted as the dealer.

– Our intention was to try out the new platform and see how it could improve our internal processes that are quite labour intensive. The platform itself is well designed and intuitive to use. Next, we will explore the API integration and remain optimistic about using the platform in future trades as well, says Palviainen.

Since Origin started developing their platform in 2015, it has gained 95 issuers and nearly 1000 active users.

– Currently, the platform is mostly for plain vanilla and callable fixed rate transactions, but we hope to see more possibilities in the future. Overall, we are happy with the test trade, Palviainen says.

Taking advantage of the constructive market tone, MuniFin announced the transaction on Tuesday 26 October at 9:10 London time. The books opened with price guidance at UKT 09/24 +30bps area. The size was fixed from the outset at GBP 250 million. The orderbook grew steadily and was finally closed in excess of GBP 300 million at 12:15.

Central banks and official institutions took 44% of the orderbook, with Asset Managers as a close second with 42.9% participation. Geographically, European investors took 54.2%, excluding the Nordics. Asia Pacific took 34% and Africa and the Middle East 10%.

– We are excited to have issued our inaugural green bond in the GBP market and to have been able to offer the green bond product to the Sterling market. It was great to add a fourth currency to our green bond offering and to further diversify our green bond investor base. We are humbled by the vote of confidence from our investors and we couldn’t be happier, says Karoliina Kajova, Senior Manager at Funding and Sustainability at MuniFin.

MuniFin has previously issued EUR and USD green bonds in the public market and one private placement in AUD. The first green bond was issued in 2016. With this transaction MuniFin is close to completing its funding target for the year.

0.875% annual, Actual/Actual (ICMA), following unadjusted

Pricing Date:

26th October 2021

Payment Date:

02nd November 2021

Maturity Date:

16th December 2024

Benchmark:

UKT 2 ¾ 09/07/24

Benchmark Spread:

+30bps

Joint Bookrunners:

BofA Securities, Nomura, TD Securities

Comments from the bookrunners

“Huge congratulations to the Municipality Finance team for navigating the volatile backdrop and printing a hugely successful, second GBP transaction of 2021. Excellent to see the issuer benefiting from the growing demand for ESG assets in GBP and adding a fourth currency to their Green bond offerings. The orderbook is testament to the strong following MuniFin has gathered amongst the UK investor base, as well as the broader global central bank community. “

Adrien de Naurois, Managing Director, Head of DCM SSA & EMEA IG Syndicate, BofA Securities

“Nomura was delighted to support Municipality Finance’s inaugural Green outing in the Sterling market – a resounding success, broadening MuniFins’s ESG investor universe and reinforcing the sustainability commitment of the organisation.”

Mark Yeomans, Managing Director, SSA Debt Capital Markets, Nomura

“Congratulations to the MuniFin team on a fantastic inaugural GBP Green transaction. There was notable participation from dedicated green investors in this trade; a clear vote of confidence from the market in MuniFin’s credentials in the ESG space. This transaction has added a fourth currency to MuniFin’s green offerings and helps further expand their green investor base.”

Laura Quinn, Managing Director, Head of Primary Markets, TD Securities, Dublin

Further information

Joakim Holmström

Executive Vice President, Capital Markets and Sustainability, MuniFin

+358 50 4443 638

Antti Kontio

Head of Funding and Sustainability, MuniFin

+358 50 3700 285

Karoliina Kajova

Senior Manager, Funding and Sustainability, MuniFin

The city had been deliberating on different power plant solutions for a long time. The city’s district heating was dependent on a single power plant and peat as fuel. Peat has become more and more expensive, which has caused upward pressure on the prices of district heating. This made it necessary to look into new alternatives.

Different kinds of waste incinerators and bigger power plant solutions were compared. In 2018, the decision was made to decentralise production to several smaller facilities instead of one large facility. A biofuel plant that will produce heat for half the city will begin its trial runs in autumn 2022. The plant was funded with MuniFin’s green finance.

“We decided not to put all our eggs in one basket. The new facility will secure the reliable production of renewable energy but will also leave room for other solutions”, says Mikko Mursula, head of district heating unit at Seinäjoen Energia.

The company updated its strategy a year after deciding on the decentralisation of production. This included setting the strategic goal of carbon neutrality by 2030.

“Until then, we did not have any concrete steps laid out ahead besides the new Kapernaum heat plant, nor did we have a clear timetable for the reduction of peat use”, Mursula says.

The fuel used in the new Kapernaum heat plant comes from different kinds of sawmill and forest felling by-products such as tree bark, sawdust and forest chips. What sets the plant aside from the rest is that it can utilise even very moist wood – the wood that is burned can have a moisture content of up to 65 per cent. There is no need to dry out the wood in piles when even freshly felled wood burns efficiently in the incinerators of the facility. The heat from flue gases is also recovered.

“While it’s not a new innovation in the industry, we are implementing flue gas heat recovery for the first time. Using modern technology, our plant now puts out 40-degree flue gas instead of the previous 150 degrees.”

An investment of more than EUR 30 million, the boiler project also includes the already completed fuel reception and processing systems. It also serves the old peat boiler.

“The new logistics already began to generate savings last summer when we started burning wood instead of peat in the old boiler.”

Heat pumps in a key role

The new heat boiler is not the only thing moving Seinäjoen Energia closer to carbon neutrality. A new auxiliary plant in Hanneksenrinne which uses pellets instead of oil was completed in 2020. In the near future, total investments will reach about EUR 60 million. It is estimated that carbon dioxide emissions will drop from the nearly 660,000 tonnes in 2018 to below 14,000 tonnes by 2023. For customers, the investments mean steadily priced and clean renewable energy.

“We have mapped out the options and aim to increase everything else except combustion-based production. Even CO2-free combustion may be unacceptable in energy production in the future”, Mursula ponders.

A new data centre being built in Seinäjoki will produce about 10 per cent of the city’s district heat supply. This is roughly equivalent to the annual demand of all the city’s single-family houses. If all goes as planned, the data centre can eventually produce heat for one third of Seinäjoki. Seinäjoen Energia has been involved in the project over the last few years.

“The data centre is designed to operate on renewable power. The heat of the data centre is recovered with heat pumps and transferred to the district heating water. Green electricity in, green heat out”, Mursula describes.

Heat pumps have an even bigger role in Seinäjoen Energia’s work towards carbon neutrality. Heat recovery and the more extensive utilisation of waste heat are being canvassed. Wastewater heat recovery could provide as much as 10 per cent of the city’s energy demand in the future. A project by EPV Energy involving the construction of a new district heating battery and electric boiler in connection to the Seinäjoki power plant is due for completion in 2022. EPV also provides wind energy for Seinäjoen Energia.

“The energy sector and the electricity market are undergoing quite an upheaval. Wind energy production is growing. Sometimes there is an oversupply of electricity, sometimes the supply does not meet the demand. On freezing winter days, the energy demand in Seinäjoki can double. The district heating battery enables us to store energy when there is excess supply”, Mursula explains.

The Government’s aid and taxation policy encourages businesses to make the green transition and heat pump investments.

“There has been uncertainty regarding the viability of heat pump investments. Investment aid speeds up investments and reduces the related risks. At the moment, investments are very profitable also due to the low interest rates”, Mursula adds.

The mandate for the EUR 500 million Social bond tap was announced 12:00 CET on Monday 4 October 2021 and the books opened the following morning with a spread guidance of mid-swaps +1 area. Exceptionally strong investor demand allowed MuniFin to tighten the spread guidance quickly to MS-1 bps area. Despite the tightening of 2 bps the orderbook grew to EUR 1.8 billion. The final spead was set to MS-2. The original bond offers a 0,050% coupon. The transaction was jointly led by DZ BANK, NatWest Markets N.V., SEB and Société Générale.

The bonds were distributed to a high degree of quality investors across Europe, with 75% placed with dedicated ESG accounts. A total of 43 investors, all European, finally participated in the transaction. Asset managers took the bulk with 43% allocation, followed by a 31% allocation to central banks and 24% to bank treasuries.

The record-high demand among ESG investors fortifies MuniFin’s excellent reputation as a sustainable bond issuer.

“We are extremely pleased with the outcome. The exceptionally high interest among ESG investors and a meaningful greenium, or should we say socium, of around 2 basis points shows that sustainability really pays off”, says Antti Kontio, Head of Funding and Sustainability at MuniFin.

MuniFin’s social finance promotes investments that produce widespread social benefits and serve the needs of their users in an exemplary way. MuniFin’s social finance projects promote equality, communality, safety, welfare, or regional vitality.

DZ BANK, NatWest Markets N.V., SEB, Société Générale

Comments from the bookrunners

“DZ BANK as an institution that firmly roots in the cooperative and sustainable financial sector is proud to have been chosen to support MuniFin in this highly successful bond issue as a bookrunner.

While we expected strong participation from Germany already ahead of the transaction, it is even greater so see how well known MuniFin is by the German investor base and how much it likes the MuniFin credit. MuniFin also met the sweet spot of demand with their 15 year tenor.

The social format of the bond and Munifin´s social commitment in the eligible categories social housing, welfare and education was another driver for the strong outcome and tight pricing of the transaction.”

Kai Poerschke, Head of SSA Origination at DZ BANK

“A great outcome for the Munifin team who remain at the forefront of ESG in the primary markets. By offering investors an opportunity to be involved in a more liquid issuance they have once again been rewarded with strong demand from a loyal investor base. Books over 3 times subscribed with a sizeable ‘greenium’ clearly show this. 75% take up from ESG accounts is another impressive statistic and represents the largest ESG allocation MuniFin have seen.”

Kerr Finlayson, Head of FBG Syndicate at NatWest Markets

“We congratulate MuniFin on the fantastic outcome of their second venture into the Social market. The transaction was met with the solid investor support that the MuniFin name always delivers, with a multiple times oversubscribed book, and pricing 1 bp inside fair value. The successful outcome today highlights investors’ commitment to MuniFin and the important work they do to improve social well-being in Finland.”

Rebekah Logan Bray, Senior Originator, SSA Origination at SEB

“MuniFin’s best in class social bond framework and investor reporting have once again been endorsed with this remarkable success. By adding liquidity to its 2035 issue, MuniFin has achieved a pricing through secondary with a transaction over 3 times oversubscribed.”

Olivier Vion, Head of SSA Primary Markets at Société Générale

Further information

Antti Kontio, Head of Funding and Sustainability, MuniFin Tel. +358 500 3700285

Joakim Holmström, Executive Vice President, Capital Markets and Sustainability, MuniFin Tel. +358 50 4443 638

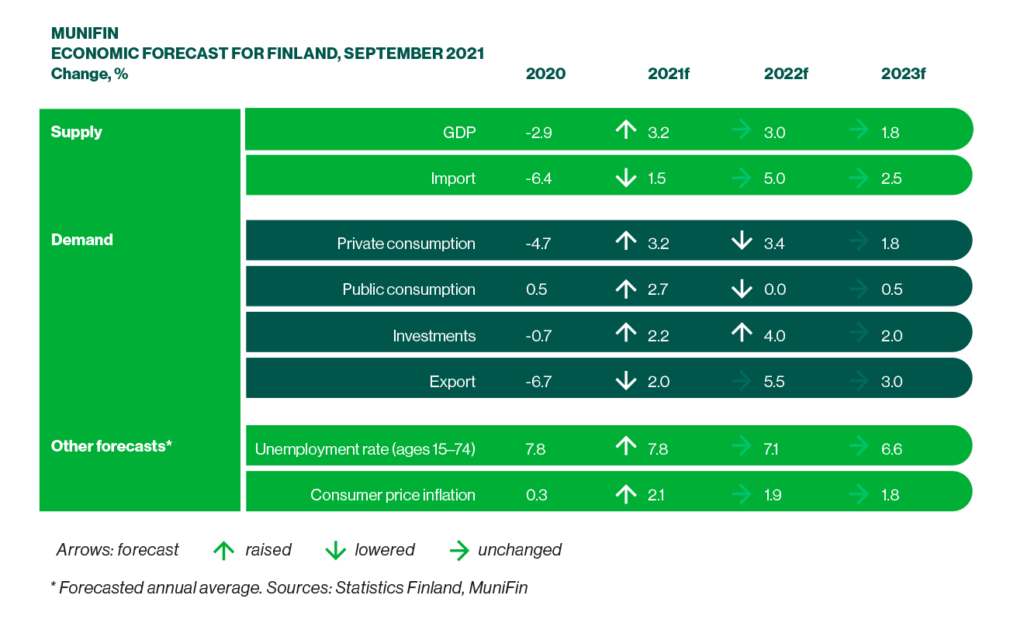

Domestic demand has recovered rapidly after the COVID shutdown period in March, says Chief Economist Timo Vesala in MuniFin’s third economic forecast this year. Finland’s GDP bounced back to pre-pandemic levels sooner than expected and investing activities have recovered rapidly as well.

As economic growth has exceeded expectations, MuniFin raised its forecast of this year’s GDP growth to 3.2%. MuniFin predicts this year’s GDP growth to carry over and stay at 3.0% in 2022, and slow down to 1.8% in 2023.

Things are looking somewhat less stable globally: forecasts for the global economy estimate that peak growth may already have passed. Vesala points out that this does not automatically imply a dramatic change in the global economic outlook.

”Overall recovery from the pandemic happened in a more front-loaded manner than expected. On the other hand, supply side bottlenecks in global value chains may have been underestimated”, Vesala explains.

Employment figures boosted by part-time jobs, recovery of overall working hours still underway

Recovering employment has been a positive surprise this year. The trend of the employment rate has already reached the pre-pandemic top level of 72.7%, and a record number of open jobs remain available.

Vesala notes that the employment figures can be explained by growth in part-time jobs. Total working hours still amount for less than before the pandemic. In other words, work is now divided among more people.

As a flipside of rapid economic recovery, significant bottlenecks have developed in the labour market. Many sectors are affected by acute labour shortage hampering growth in production.

“Part of the shortage is due to a skills gap. Jobs lost during the pandemic are being replaced with new, but slightly different ones with different skill requirements”, Vesala observes.

Economic recovery may increase regional differences

The demand for labour has regional differences. Southeast Finland and North Karelia have fewer open jobs per capita than the Finnish average, while South and Central Ostrobothnia, Kainuu and Lapland have more. The demand for labour has grown even faster in municipalities and joint municipal authorities than in the private sector.

Labour shortage is evident especially in Ostrobothnia, where unemployment is substantially lower than the average in Finland. Kainuu and Lapland are suffering from a particularly difficult employment mismatch where many jobs are available, but unemployment remains high.

As the economy recovers, these kinds of regional differences may become larger.

“The regions with an educated and economically active population will reap the most benefits from the economic upswing”, Vesala predicts.

Uncertainty about the health and social services reform

The improving economy has a positive effect on municipal finances as well. Employment and total payroll have grown faster than expected, resulting in more tax income. Esa Kallio, CEO at MuniFin, points out that favourable economic conditions alone will not solve the structural challenges that municipalities struggle with.

“Transforming age structure and dwindling working population continue to threaten the economic sustainability of many municipalities.”

Implementing the health and social services reform is also a burdensome execise for municipalities.

“There is uncertainty about municipality-specific impact assessments and transfer of functions. At the same time, municipalities are expected to determine their post-reform level of taxation for the year 2023. This is a very difficult task. And while the reform reduces some need for municipal investments, it shrinks municipalities’ operations much more in comparison and thus a smaller income base supports investments. Supporting the long-term investing capacity of municipalities is therefore even more important than before”, Kallio summarises.

MuniFin’s ultimate objective is to embed sustainability across all its business areas. Treasury has further set concrete sustainability targets for its investments. The Framework is a transparent way to communicate these targets and principles to all our stakeholders, such as customers, investors and ESG rating agencies.

“Sustainability is in our DNA at MuniFin. This is evident in our core business, as our mission is to develop the Finnish welfare state, and in our tradition of being an active issuer of sustainable bonds. Now we want to strengthen our role as a responsible institution by publishing our own framework for sustainable investing”, says Pasi Heikkilä, Head of Treasury and Capital Markets Services.

The new Sustainable Investment Framework is one important step on MuniFin’s sustainability roadmap.

“We work hard to develop our operations in line with our strategy and values of which sustainability is a key element. The creation of Sustainable Investment Framework is part of the systematic work we carry out. We aim to increase the transparency of our investment management and promote sustainable investment practices. Simultaneously, we acknowledge the increasing importance of ESG risks that should be considered in managing our investments. This is the next step and we will continue walking”, says Kalle Kinnunen, Sustainability Manager at MuniFin.